In September, Jenn referred me to the Marriott Bonvoy Boundless card, and there was something odd about the offer that was sent me. If I applied for the card without a referral, I would have gotten 3 50,000 point certificates after spending $3,000, because that was the standard advertised deal at the time so that’s the deal I was expecting to get when she referred me. Instead, what I was offered was 3 35,000 point certificates after spending $1,000. Lower spend, lower reward, but Jenn would get a 40,000 point bonus. We talked about it for a while and determined that we could get a vacation rental from Marriott Homes and Villas for less than 35,000 points per night (obviously now we know you can’t book those on certificates). We went ahead and took the referral offer, because the extra 40,000 points were very nice to have.

We also pulled the trigger on the Hyatt Ziva Los Cabos. I had left a 2 day window open on our trip to Los Cabos. It really shouldn’t have made me nervous, but it did. Every day I was worrying that we wouldn’t be able to book it when I finally had the points in hand. But, I got my bonus and was excited to book it. I logged on, put the two days in my cart and went to check out and it told me that I didn’t have enough points. As it turns out, Friday was 20,000 points and Saturday was 23,000 points. I expected them to both be 20,000 points, so I didn’t quite earn enough points. I briefly considered waiting another month, spending the necessary $1,000 on my World of Hyatt card to get the necessary 2,000 points. Forget it, just buy the points and book the room. It cost me $48 to buy the 2,000 points, I was okay with that even though it pained me a little to buy points.

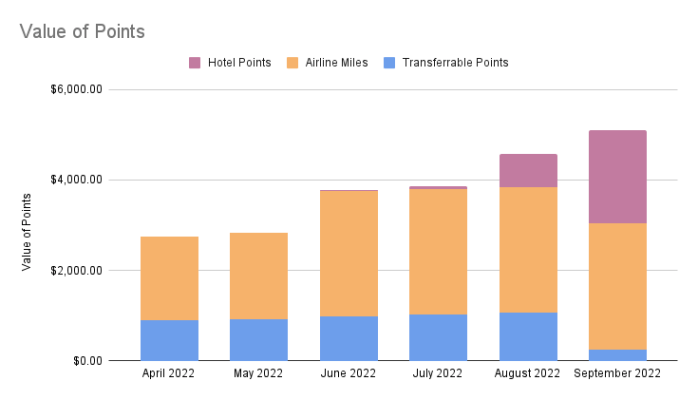

On to the point check!

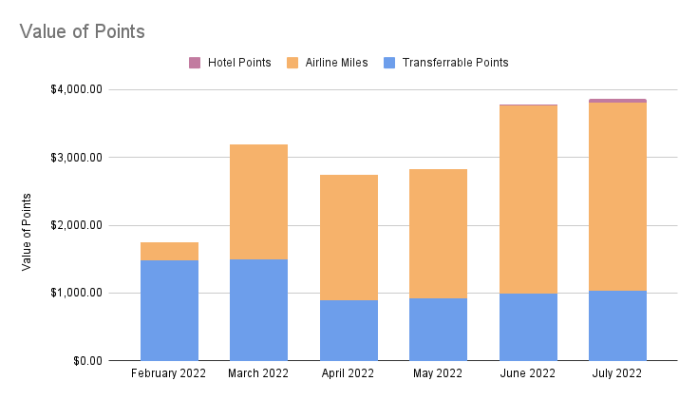

I spent around $600 on my Chase World of Hyatt card and earned about 600 points. I spent around $2,200 on my Citi Premier card and earned 2,600 points. Jenn spent $3,500 on her Marriott Bonvoy Boundless card and earned 8,600 points for that. She referred me to the Marriott Bonvoy Boundless card and received an additional 40,000 points and she got her 5 50,000 point certificate bonus. I redeemed 43,000 Hyatt points for 2 nights at the all-inclusive Hyatt Ziva Los Cabos but I was a little short so I had to buy 2000 points for $48.

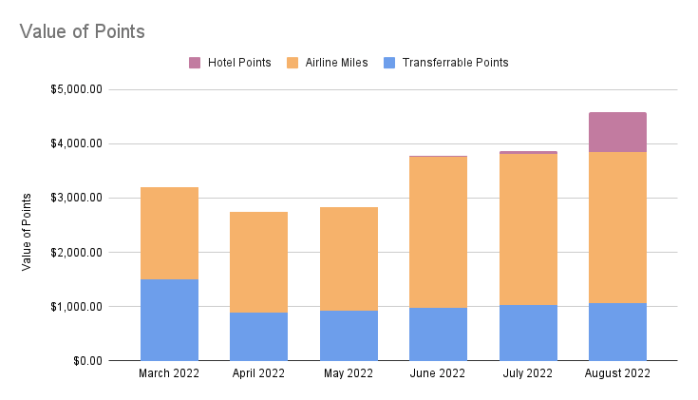

At the end of the month we sat at 245,900 United miles, 62,300 Citi points, 53,600 Marriott Bonvoy points, 600 Hyatt points, and 5 50,000 point Marriott certificates.

At this point, it did start to feel a little wild, this seemed like a lot to pick up in 10 months. People who have been doing this for a while know this is fairly normal, but we were new at this and it seemed crazy.