Only 5 months after redeeming almost all of our points booking our trip to Europe, we had managed to acquire enough points to almost be back to where we were. That is really amazing to me knowing that we had booked this dream vacation and before we could even take the trip, we had basically replaced the points. It makes me really excited about future possibilities.

One of the main reasons for the big jump in points value this month was that Jenn got her 60,000 point bonus from hitting her spend on her Chase Sapphire Card. I also received my $200 bonus from my Bank of America Customized Cash Back Card. I redeemed the $220 in cash back from Bank of America on 4 train tickets from Munich to Venice. I’m really looking forward to this train ride because it sounds amazing to take a train across the Alps.

Jenn applied for the Chase Business Ink Cash Card because they were still running the 90,000 point bonus (or $900 cash) for $6,000 in spending for the first 3 month promotion. The typical Ink sign up bonus is 75,000 Ultimate Reward points (or $750 cash) for spending $7,500 in the first 3 months. I’m surprised that promotion is still around after a few months, it’s a really solid promotion. The Chase Business Ink Cash Card is honestly a fantastic business card. It is a no annual fee card and it offers 5% back on office supply stores, internet, phone services and cable. It also gives 2% back on gas stations and restaurants. Technically this is a cash back card, but they give you the cash back in the form of Ultimate Reward points at 1 cent per point. If you only have the Ink Cash card then it’s only good for cash back, but if you also have a Chase Sapphire Card (which we do) or a Chase Ink Business Preferred Card then those points can be transferred to Chase’s multiple airline and hotel transfer partners. Normally you will get your best value for those points by transferring the points to a transfer partner.

I continued picking up random cash back cards for quick cash bonuses to use for expenses on our trip to Europe. I signed up for the Bank of the West Cash Back World Card. Why? Well they sent me a mailer and it is fits in with a larger strategy that I’m using right now to get cash back cards from banks that don’t have good transferable partner programs. I’m trying not to burn bonuses from really good cash back cards. What I don’t want to do, for example, is get the Citi Double Cash card where I can convert the cash back to transferable points and then use the cash, when later I might want additional Citi Thank You points. I’ll save an application for that card when I’m not looking strictly for cash. The Bank of the West Cash Back World Card has no annual fee and gives 3% back on groceries, gas and dining and 1% back on everything else. It was offering me a $200 bonus on $1,000 spend in the first 3 months.

Anyway, on to the point check!

I spent $1,300 on my Bank of America card and earned the bonus and an additional $20 back for a total of $220, which I immediately used on train tickets. Jenn spent around $2,100 on her Chase Sapphire Card and earned both 3900 Ultimate Reward points for the normal spend and 60,000 bonus points. Jenn also spent around $600 on her Chase Marriott Boundless card and earned around 1,300 points as well as $800 on her Chase Ink Cash card earning 1,000 Ultimate Reward points. I also spent around $200 on my Citi Premier Card and earned 300 Citi Thank You points.

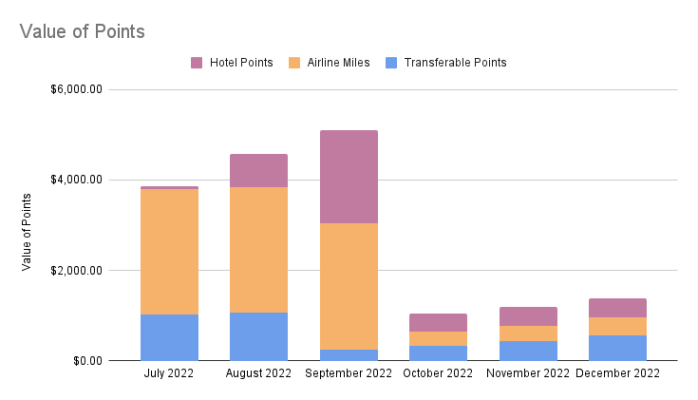

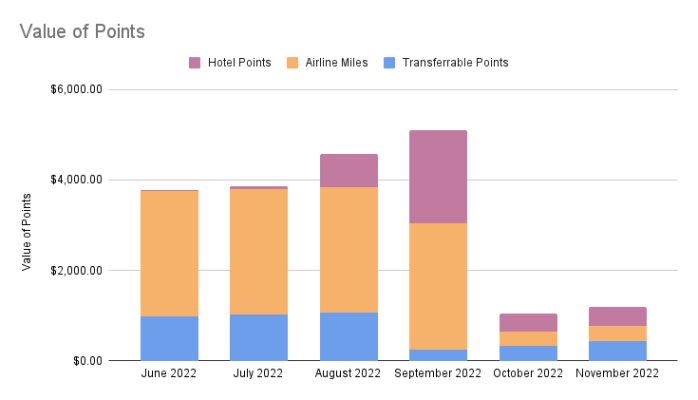

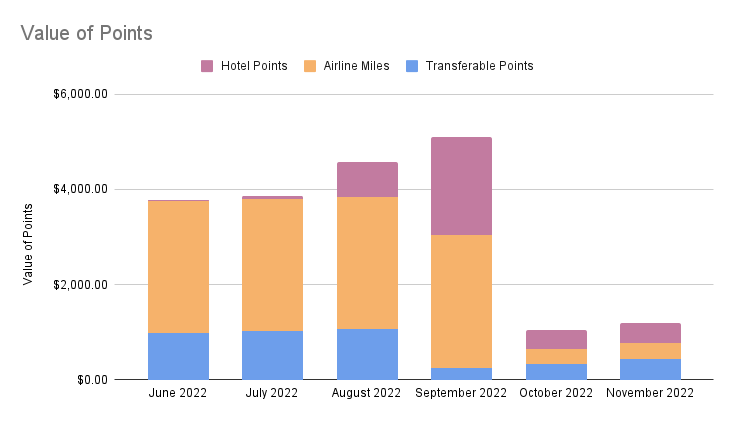

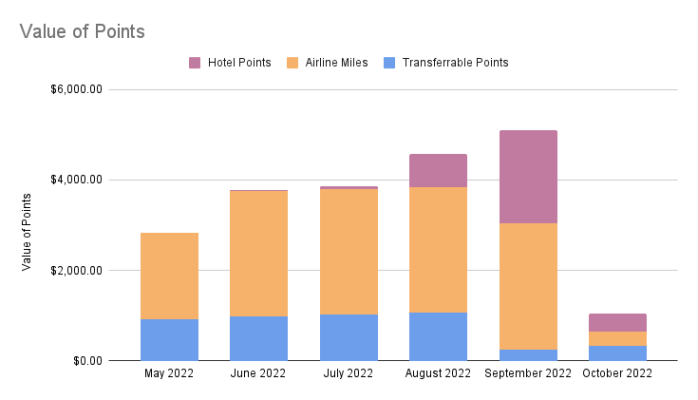

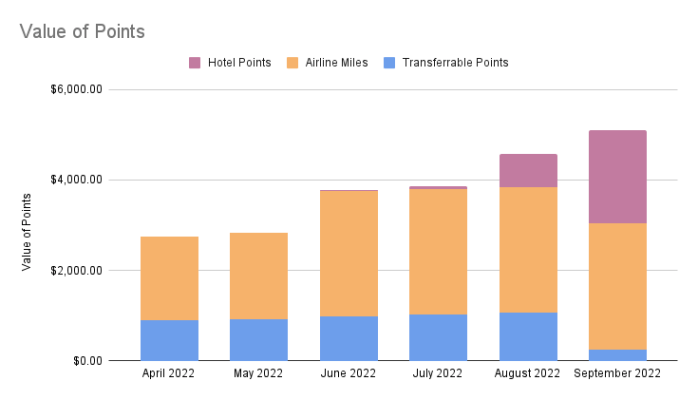

We have been piling up transferable points, mostly in the form of Ultimate Reward points which is great because of the flexibility that transferable points gives us. We finished the month with 172,600 Chase Ultimate Reward points, 51,300 Marriott Bonvoy points, 40,500 United miles, 23,700 Citi Thank You points and 1,500 Hyatt points. Using the valuations published by The Points Guy at https://thepointsguy.com/guide/monthly-valuations/, these points and miles are worth over $4,700.