February in Iowa is brutal. It’s been cold and dark. Midwestern winters are primarily about survival. You just go inside and stay. Most people binge-watch TV shows under a heated blanket. We’re not big television watchers, so we’ve been spending an unhealthy amount of time in breweries, where the Quad Cities excels in both quantity and quality. Illnesses are running rampant, as Iowans have been breathing the same indoor stale air since November. At this point, we’re all just dreaming of going outside for anything.

Because of all of this, if you go anywhere to Florida, Arizona, or the Caribbean during March or April, you will run into dozens of folks from the Midwest, in our annual desperate attempt to bookend the hellscape that is Midwestern winter. Spring break isn’t an annual tradition; it is the only thing that keeps us from tying a brick to our legs and jumping into an icy lake in the winter. WE NEED THIS!

For the last three years, we’ve planned unusual Spring Breaks. Frankly, we’ve done Florida, and I just can’t do it anymore. I don’t want to share a beach with obnoxious, drunken college students. Because of that, our Spring Breaks have been a little different lately. Two years ago, we went to Costa Rica and spent time hiking in the mountains, lying on the beach, and enjoying Costa Rican culture. Last year, we spent six days hiking the Portuguese route of the Camino de Santiago. This year, we will visit the Canary Islands, specifically Tenerife Island, which is part of Spain, but off the coast of Africa. This will give us a beach vacation, but without the crowds of Florida and the Caribbean. We will also be stopping in London and Madrid as part of this trip.

Spring Break couldn’t come soon enough, because we are starting to lose our minds here, and it’s time for us to go outside and get some vitamin D.

Atmos Awards Ascent Visa Card

We said we weren’t going to do this. We were going to take it easy and sign up for fewer cards this year, but alas, Jenn signed up for the Atmos Awards Ascent Visa Signature card. This is while I’m working on a signup bonus for my Iberia Plus card, and Jenn is working on a signup bonus on her Bilt Palladium Card.

There was a valid reason for this: Jenn wants to plan a girls’ trip with her and Emma to celebrate Emma turning 21 and is considering options in the Northwest, including Seattle, San Francisco, or Portland. Atmos miles would work really well for any of those destinations, and now that she earns Bilt points, she has a way to top off the account by transferring Bilt points to Atmos. It’s always a good idea to pair a hotel or airline card with a transferable points card to have some flexibility and top off an account. Having the Bilt card makes the Atmos card more attractive.

The Atmos Awards Ascent Visa Card has a $95 annual fee and earns 3X on Alaska Airlines purchases, 2X on Gas, EV charging, transit, rideshare, cable, and streaming services, and 1X on all other purchases. If you spend $6,000 in a year, you will earn the companion fare, which allows you to book a companion flight for $99 plus taxes.

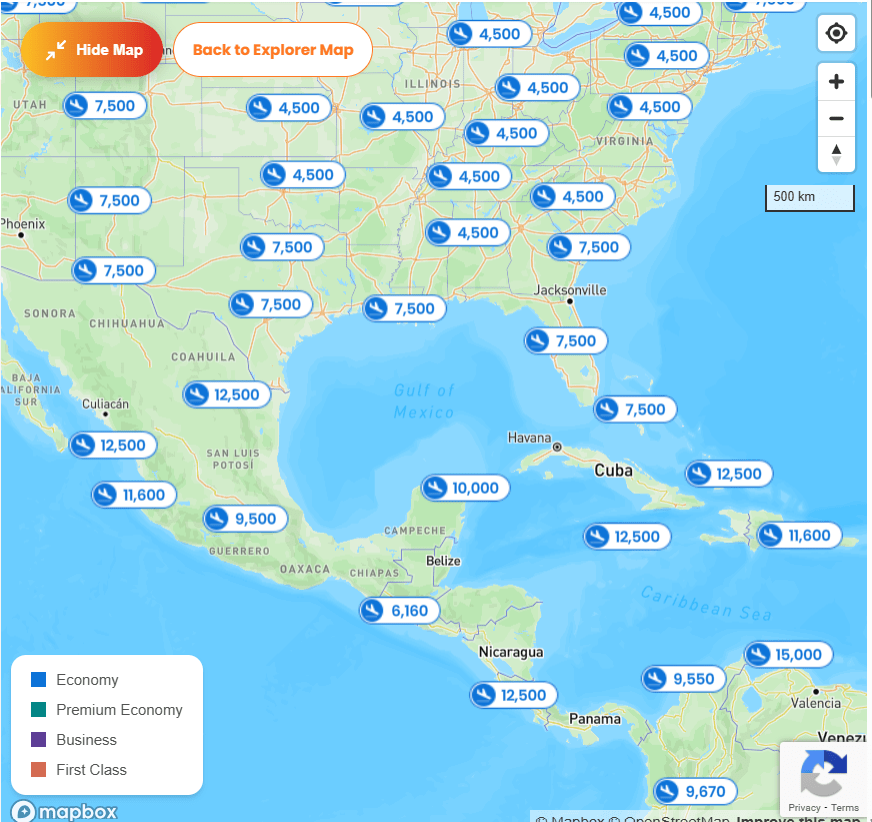

The current bonus for this card is 70,000 points when the cardholder spends $4,000 over the first 90 days. The Atmos Awards program is known for strong partner booking rates. Short-haul domestic flights on American Airlines typically cost 4,500 points, and I see many routes to Europe for 27,500 points with minimal fuel surcharges. Having a few more Atmos miles will be a good thing to have around.

UK Electronic Travel Authorization

Since 2025, the UK has required an electronic travel authorization to enter the UK from the United States. This is to enhance their border protection. Each application costs 16 British pounds and, if approved, is good for two years. On their website, they say to allow up to three business days to process the application, so you need to plan ahead.

This will be our first trip to England, and while I’m not happy about the fact that I have to pay for four authorizations costing a total of $90, we went through the process and found it to be fairly easy. We used the phone app to apply, and I think that might be the reason. Using an iPhone, it was able to scan our faces, scan our passports, and take photos of us and our passports. Scanning the passport was interesting; apparently, there is a chip in the back cover of your passport, and it was able to read it through the phone.

Anyway, this process took just a few minutes, and we were approved immediately. There is an option to apply online, and I assume that you would not be able to scan the passport or your face, and maybe when you apply that way it takes them longer to verify the information. That might be why we were approved instantaneously and they say to allow three business days. So if you do have an emergency trip to the UK, I would use the app, I think that will give you a better chance of instantaneous approval.

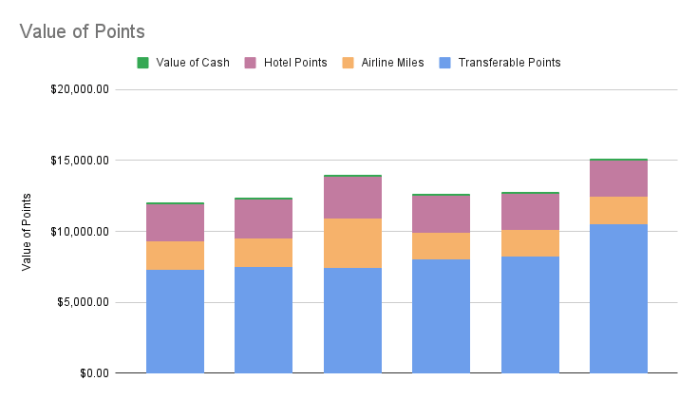

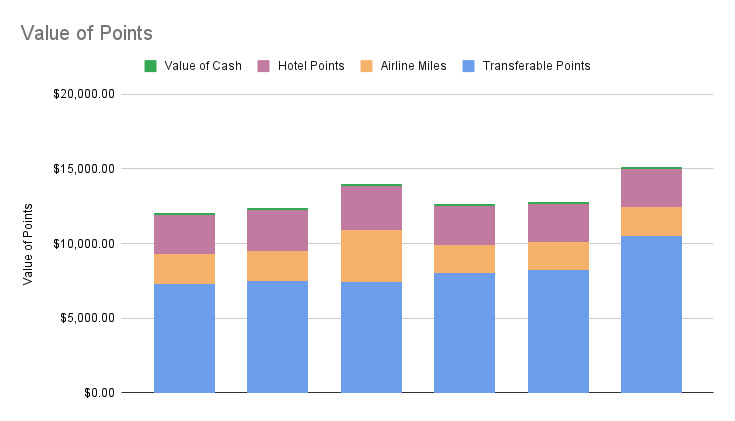

On to the Points Check

We spent around $2,500 on cards not earning a bonus, earning less than 5% return on that spend. That’s below where I want to be. I want to shift as much of this to the Bilt Palladium card over time, since that has solid earnings on all spend. I’m going to continue to keep utilities on the Wyndham Business Earner card since it earns 5X on utilities, and I’ll keep our phone bill and streaming services on the Ink Cash since it earns 5X on that spending. But other than that, most of this would be better spent on the Bilt Palladium Card.

| Card Used | Spend | Points Earned | Point Value | Points Per $ | Return on Spend |

| Amex Gold | $1,333 | 2,619 | $52.38 | 2.0 | 3.9% |

| Sapphire Preferred | $508 | 772 | $15.83 | 1.5 | 3.1% |

| Ink Cash | $441 | 2,204 | $45.18 | 5.0 | 10.3% |

| Ink Unlimited | $101 | 153 | $3.01 | 1.5 | 3.0% |

| Wyndham Business Earner | $84 | 420 | $4.62 | 5.0 | 5.5% |

| Blue Business Plus | $66 | 132 | $2.64 | 2.0 | 4.0% |

| Total | $2,533 | 6,300 | $123.71 | 2.5 | 4.9% |

Aside from the spending above, I spent a little over $1,600 on my Iberia Plus card, earning 1,600 Avios, and Jenn spent a little over $1,600 on her Bilt Palladium card, earning almost 4,600 Bilt Points. We used $200 in Bilt Cash to activate the Points Accelerator, which adds an additional 1 point per dollar spent on the next $5,000 in spend. That essentially makes the Palladium Card a 3X anywhere card.

That leaves us with a total of:

- 327,000 Chase Ultimate Reward Points

- 247,300 IHG Points

- 175,800 Amex Membership Rewards Points

- 101,200 Wyndham Points

- 79,400 Alaska Miles

- 33,900 American Airlines Miles

- 19,300 Citi Thank You Points

- 16,700 United Miles

- 15,900 Marriott Bonvoy Points

- 4,600 Bilt Points

- 1,600 Avios

- 1,500 Delta Miles

- 300 Hyatt Points

- $133 Cash Back

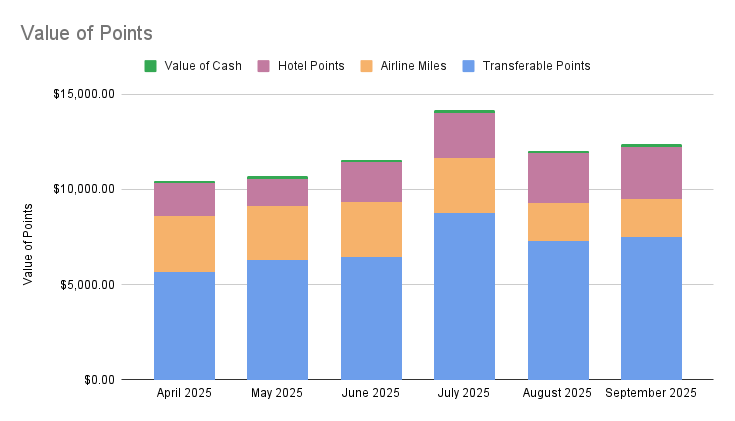

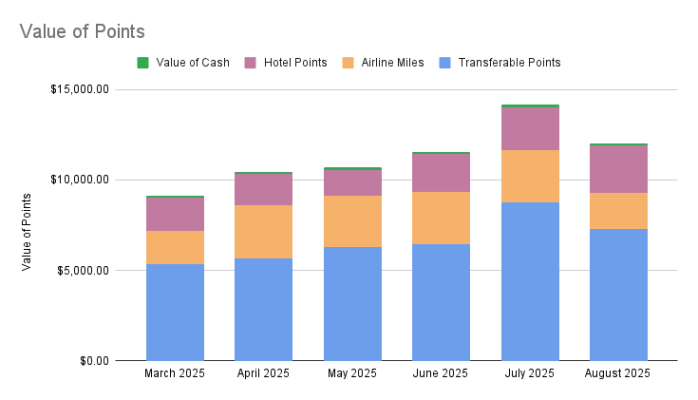

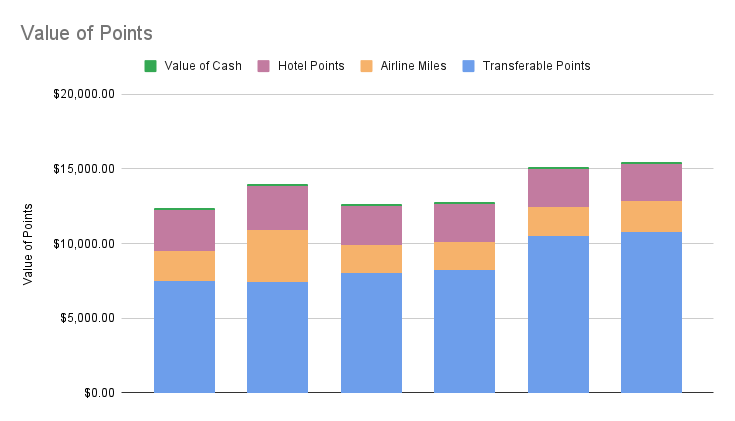

All of this, using the points valuations published by The Points Guy, is worth a total of $15,300. That’s the highest it’s been in a while, which is great, but right now I’m a little more focused on getting out of this winter hellscape and getting to a beach. I can’t wait to get to Tenerife.