Life sometimes pulls you away from your hobbies. That’s okay, since your hobbies are really there to fill in the time that remains from your real life. Our real life has been overfilled lately. Our daughter, Emma, moved out in June, and the process of her moving out continues today and may continue for months to come. Our son, Alex, is visiting college campuses, with a completed visit to the University of Illinois and upcoming visits to the Universities of Wisconsin and Michigan. As an Iowa Hawkeye fan, it’s tough for me to be objective about other Big Ten schools, because I hold some pretty deep-seated resentments toward their athletic programs. But, alas, this is about his education, not about my inability to cope with the Hawkeyes losing to Illinois in the Elite 8 last year.

Oddly enough, the first campus visit we ever did was in Berlin at the International University of Applied Sciences, where we did a quick self-guided tour. The ‘campus’ was pretty sad, and I immediately walked out and said to Alex, “So, I’m guessing that’s a ‘no’ on this college.” To be fair, he wasn’t seriously considering it, but we were in Berlin, their curriculum was interesting, it was taught in English, and the price was really good. I mean, it’s almost cheap enough to consider going to school there just for the temporary residence permit.

Things that Hurt My Butt

Aside from school visits, we’re not planning or doing much. Our friends Bill and Theresa did get us out to Iowa City one weekend to do the Big Rove bike ride, which is around 40 miles total, and you can choose to ride from either the Big Grove Brewery in Cedar Rapids or Iowa City to the Big Grove Brewery in Solon, Iowa. Bill was deep in training for RAGBRAI, the annual bike ride across Iowa. If you’re unfamiliar with RAGBRAI, it stands for the Register’s Annual Great Bike Ride Across Iowa. It usually has around 20,000 riders and is a weeklong event that changes routes each year. It is typically around 400 miles long and is perhaps the most unique bike ride in the country.

Bike stop at Big Grove Brewery in Solon Iowa

Because of RAGBRAI training, Bill had spent a considerable amount of time on his bike this year, while I had not. This meant that my butt was considerably sore, since I hadn’t conditioned it to my seat, while Bill was practically doing a warm-up ride. It was a great ride, though, even though it was surprisingly hilly. Maybe next year we’ll ride from Cedar Rapids to Solon instead of Iowa City to Solon.

The lobby of the Graduate features a bunch of bookcases with the spines of the books turned in instead of out.

We decided to spend two nights in Iowa City so that we could stay the day before and the day after the ride. We used our $200 Bilt Hotel Credit and $100 in Bilt Cash to wipe out the vast majority of the cost of our two-night stay at the Graduate Hotel. That hotel is really quirky, right in the heart of the pedestrian mall in Iowa City.

Typically, the Graduate has hotel rates in the low $100s per night, but for these nights they were a bit elevated. Before we arrived, we couldn’t figure out why the hotel’s rates were so much higher than usual (about 30%- 40%). It turns out there was a giant block party going on in the pedestrian mall that weekend, so I suspect that was the reason. It’s definitely not a luxury hotel, but I’ll take quirky over luxury anytime, so I’m sure we will return to the Graduate – especially since the location is great.

An Eye on Next Summer

We haven’t been spending much time thinking about points and miles lately. I think it’s actually been quite a few months since we’ve chased a signup bonus. That being said, I’m trying to plan ahead for a trip next summer for Alex’s graduation trip. He’s indicated that he wants to go to Iceland and/or Finland (we told him probably ‘or’ since both of those places are expensive). I’m thinking that we should spend three or four days in one of those places, then head south in Europe, where the food is more edible and considerably cheaper.

Looking ahead, we have some good options, with a decent amount of Alaska miles, American Airlines miles, and Avios. We also have the option to boost those with transferable points, since we can transfer Bilt to Alaska Airlines, Citi Thank You points to American, and Chase, Citi, Bilt, Amex, and Capital One to Avios. As we get closer to booking those flights, we will be concentrating on building points balances in those programs.

On to the Points Check

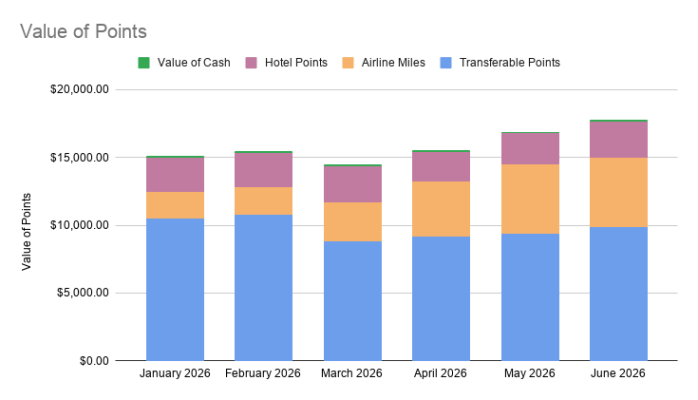

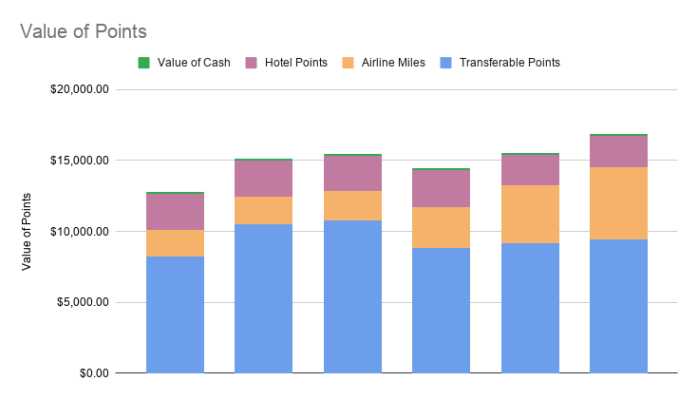

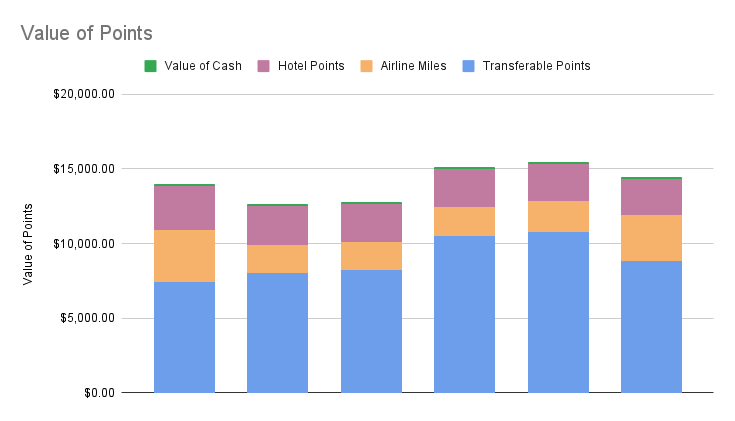

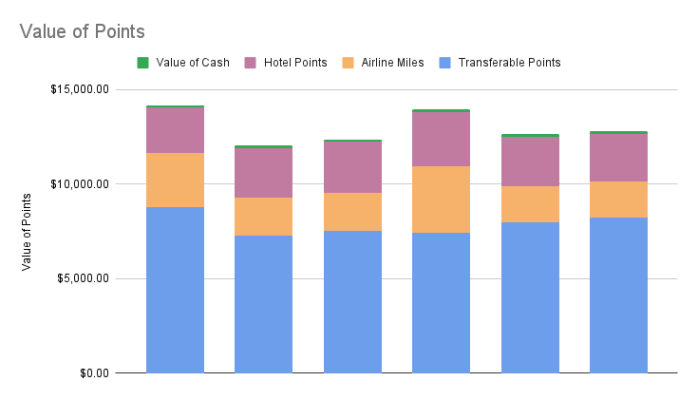

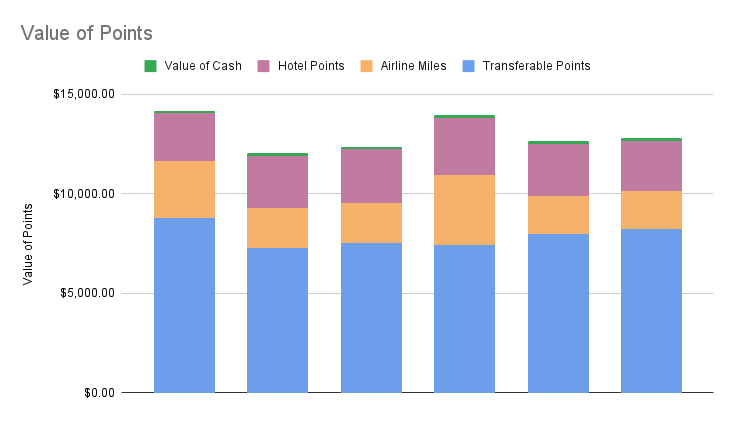

We’ve hit an all-time high again. This was routine before, but we had a high in October of 2024, when our points were worth a total of $16,500, and then we had a series of trips that ate into those totals. Since then, we’ve visited Portugal, Spain twice, England, France, Germany, and Ireland. Now that we’ve slowed down a little, we’re reloading our point totals, and I’m looking forward to spending these when Alex scurries on to college. I love my kids, but I’m looking forward to traveling without them and not having to work around their school schedules.

One of our Marriott Bonvoy Brilliant cards just hit its annual fee, which means that we have a shiny new hotel certificate. I value it at half of the maximum value of 35K points and hope that I can use it for better value than that. That means that I value the certificate at around $140, which exceeds the $95 annual fee. As long as I’m using that certificate, there’s no reason for me to cancel that card.

Card Used

Spend

Points Earned

Point Value

Points Per $

Return on Spend

Bilt Palladium

$3955

13,309

$292.80

3.4

7.4%

Custom Cash

$868

2,869

$54.51

3.3

6.3%

Ink Cash

$460

2,302

$47.19

5.0

10.3%

Wyndham Business Earner

$407

2,037

$14.26

5.0

3.3%

Ink Unlimited

$406

610

$12.20

1.5

3.1%

Amex Gold

$363

600

$12.00

1.7

3.3%

Total

$6,459

21,727

$432.96

3.4

6.7%

This month’s spending not devoted to earning a signup bonus

Since we’ve had no new credit cards that we are working on a signup bonus for, we’ve primarily been using our Bilt Palladium card for our everyday spend. The other cards were primarily used for their bonus categories, although some charges could have been used on a more advantageous card. Overall, a 6.7% return on spend is tremendous for non-bonus spend.

After this month’s earnings, we are left with a total of:

263,200 Chase Ultimate Reward Points

230,650 IHG Points

156,600 Alaska/Hawaiian Airlines Atmos Miles

123,800 Wyndham Points

94,900 Amex Membership Rewards Points

92,600 American Airlines Miles

88,500 Bilt Points

81,800 Avios

33,700 Marriott Bonvoy Points

27,600 Citi Thank You Points

19,300 United Miles

1,500 Delta Miles

300 Hyatt Points

$133 Cash Back

Those point totals, according to the valuations published by the Points Guy, add up to a grand total of $17,800. This is our all-time high, and without any immediate plans to do any extensive travel, we should continue to build on this total. I need to start focusing on what kinds of points are necessary to plan our trip next summer, so I’ll probably be looking for ways to add some airline miles soon.

In the Points and Miles community, most of the discussions are based around how you can use points and miles to maximize epic trips. This can be done by redeeming those points and miles for luxury hotels and business-class lie-flat seats to exotic destinations. But what if you travel mostly by staying in exotic hotels like the Comfort Inn in Kokomo, Indiana, or the Holiday Inn Express in Bettendorf, Iowa?

I’m talking about travel sports parents, the utterly exhausted parents who drove hours to sit in the sun all day and watch game after game at some regional youth sports tournament. I remember when my daughter played on a club basketball team, and while their team didn’t travel too much, I was constantly having conversations with other team parents whose kids were in other sports and were traveling seemingly every weekend. They were exhausted and broke.

How could using points and miles save them money on all of those hotel stays? Typically, I would suggest getting a Hyatt or Marriott credit card, which could give you free nights through points or free night certificates. The problem with that is, travel sports parents don’t get to choose the hotel, well, at least if you don’t want your kid to hate you. Usually, the team stays at the same hotel since the kids want to hang out together after the games. This means you are probably going to need to be more flexible, and this could mean earning points that can be used in a travel portal as well as using hotel credits in those portals.

Bilt has three credit cards that not only earn Bilt Points that can be used in their travel portal but also Bilt Cash, which can be used for hotel credits (although it’s limited). You can use Bilt Cash and Bilt Points in combination to book hotel rooms on the Bilt Travel Portal. Using Bilt Cash for long stays isn’t too exciting because, depending on your Bilt Status, you can only use $50 or $100 per month. However, if you’re only staying two nights, which is the minimum stay to use those credits, they really cut down on your hotel bill. The Bilt system works best for people who have a lot of short hotel stays, like travel sports parents.

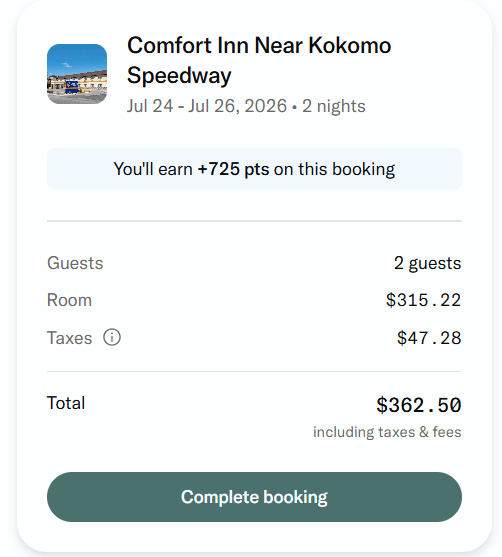

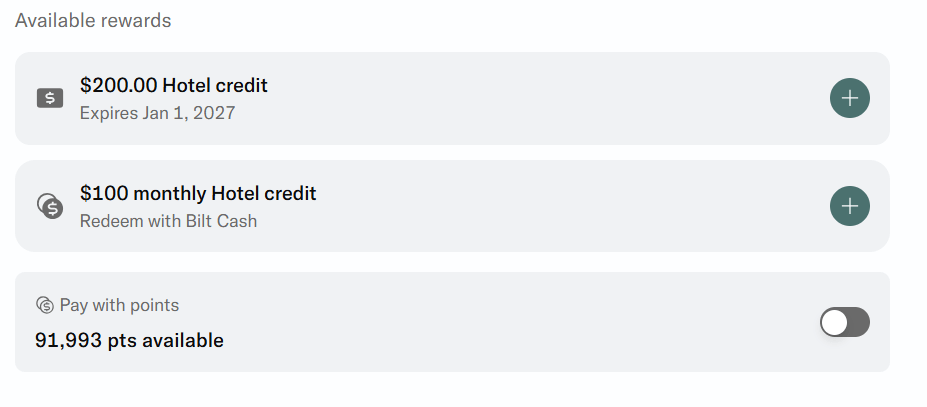

Here is how it works: the 2-night stay shown below runs $362.50. Because I have the Bilt Palladium Card, I have an available semi-annual $200 hotel credit. Since I have Gold Status, I can use $100 in Bilt Cash. I can also use points at 1.25 cents per point or pay with cash. I can also use multiple options together. For example, I could use the $200 hotel credit, $100 in Bilt Cash, and 5,000 Bilt Points to wipe out the hotel bill.

I’m going to run some scenarios that show how much a travel sports parent can save on hotel stays, using the various Bilt credit cards, and I will compare it to another good option, the Chase Sapphire Preferred card. But to understand the scenarios, I need to explain a few things about Bilt.

Bilt Status Matters

There are 4 tiers of Bilt Status: Blue, Silver, Gold, and Platinum. While you can earn your status by earning Bilt points, the easiest way is by spending on a Bilt Card. Each tier of status has different benefits, but for this discussion, I’m focusing on the fact that Blue and Silver status members can use $50 in Bilt Cash per month for hotel credits, and Gold and Platinum status members can use $100 in Bilt Cash for hotel credits. Since Gold Status is the tier where the hotel credit jumps from $50 to $100 per month, it is the important tier for this discussion. That status is earned by spending $25,000 in a year on a Bilt credit card and is good for the rest of the year and the next calendar year. Also, as part of the signup bonus for the Bilt Palladium card, Gold Status is automatically given to the new cardholder for the rest of the year and the next year.

What Bilt Cards Earn

Between the three Bilt credit cards, each has a different earning structure. Each has elevated earnings for some travel categories, but for this discussion, we will ignore that. The only bonus category worth mentioning is the 3X on either groceries or dining on the Bilt Obsidian Card. For the comparisons below, I assumed that, since we are talking about parents with athletes, they will spend $1,000 per month on groceries, and they will choose the grocery option on that card. The Bilt Obsidian Card earns 1X on everything else. The Bilt Blue card earns 1X on everything, and the Bilt Palladium Card earns 2X on everything.

Using Bilt Cash to Boost Points Earning

On each of these credit cards, the cardholder will earn 4 cents of Bilt Cash per dollar spent (in addition to Bilt Points earned). That means that if, in a month, the cardholder spends $2,000 on the card, they will earn $80 in Bilt Cash. If the cardholder has only Blue or Silver Status, they can use only $50 of Bilt Cash toward a hotel credit. That leaves an extra $30. But if you use the Bilt ACH to pay your rent or mortgage, you can earn points on your housing payments as well. You can earn points on rent or mortgage payments by paying a 3% fee in Bilt Cash. In other words, $30 in Bilt Cash can unlock points for $1,000 in rent or mortgage, which is 1,000 Bilt Points.

So in the above example with the Bilt Blue Card, the cardholder spends $2,000 and earns 2,000 Bilt Points and $80 in Bilt Cash. They use $50 in Bilt Cash for a $50 hotel credit and the other $30 in Bilt Cash to unlock an additional 1,000 Bilt Points by running their rent or mortgage through the Bilt ACH. The cardholder ends up with 3,000 Bilt Points and $50 in hotel credit.

If you still have additional Bilt Cash after using the Bilt ACH for housing credits with the Bilt Obsidian or Palladium Cards, you can use $200 in Bilt Cash on the Points Accelerator to earn an additional 1X on all purchases for the next $5,000 in spend. In other words, you can convert $200 in Bilt Cash to 5,000 Bilt Points by spending on the card.

On all of the below examples, I assume that the example person has a rent or mortgage of $2,000 per month, so they use the ACH for up to that amount and then use the points accelerator on any Bilt Cash left over after that.

Card Benefits and Annual Fees

Any signup bonuses or perks of the cards also have to be taken into consideration. The annual fee is subtracted from the amount saved, since that is an expense. Here are a few other things listed below that will affect the analysis of these cards:

Bilt Blue Card has $100 Bilt Cash Signup Bonus

Bilt Obsidian Card has $200 Bilt Cash Signup Bonus

Bilt Obsidian Card has $100 in Bilt Travel Credit ($50 every 6 months, min 2-night stay)

Bilt Obsidian Card has a $95 annual fee

Bilt Palladium Card signup bonus includes Gold Status for rest of this year and all of the next year

Bilt Palladium Card signup bonus has 50,000 points and $300 in Bilt Cash

Bilt Palladium Card has $400 annual hotel credits ($200 every 6 months, min 2-night stay)

Bilt Palladium Card has $200 Bilt Cash annually on the anniversary date

Chase Sapphire Preferred Card has $100 hotel benefit

Chase Sapphire Preferred Card has a $95 annual fee

Chase Travel Portal vs Bilt Travel Portal

In the Chase Travel Portal, you can redeem Chase Ultimate Rewards points for 1 cent per point toward a hotel stay. Sometimes, Chase does have a points boost that can make those points worth up to 1.5 cents per point, but you can’t really count on that. For this discussion we will assume a 1 cent per point redemption on the Chase Travel Portal.

For the Bilt Travel Portal, points can be used at 1.25 cents per Bilt point. Bilt allows you to combine credits and points as well, which means that if you had a $225 hotel stay, you could combine $100 in Bilt Cash and 10,000 Bilt points to pay for the room.

Scenario 1 – Cardholder Spends $25,000 per Year

For most parents who have kids in travel sports, $2,100 per month on a card will be a little on the light side, especially if you are using your credit card for utilities, insurance, gas, etc. I can’t imagine that any parent with children in youth sports isn’t spending at least $1,000 per month on groceries. So, for the comparison below, I’m assuming that $1,000 is on groceries and the rest is in other categories. Since the Chase Sapphire Preferred card has 3X categories such as gas, dining, and streaming services, but is only 1X on groceries, I’m going to assume the average will be 1.5X on everything.

The reason I chose $25,000 per year is that if you spend that amount on a Bilt card, you will earn Bilt Gold status, which will bump the amount of Bilt Cash that can be used for hotel credits from $50 per month to $100 per month. Having that dramatically changes the amount that you can save on hotel stays.

The examples below are based on the assumption that the cardholder will have hotel stays in 9 different months a year. The number of months affects how much Bilt Cash can be used for the analysis, since it’s $50 or $100 per month, depending on Bilt Status.

Card

Points Earned

Bilt Cash for Hotel Credit

Hotel Credit as Benefit

Annual Fee

Total Saved on Hotel Stays

Bilt Blue Yr 1

43,330

$450

$0

($0)

$991

Bilt Blue Yr 2

28,330

$900

$0

($0)

$1,254

Bilt Obsidian Yr 1

67,330

$450

$100

($95)

$1,296

Bilt Obsidian Yr 2

52,330

$900

$100

($95)

$1,559

Bilt Palladium Yr 1

103,330

$900

$400

($495)

$2,096

Bilt Palladium Yr 2

53,330

$900

$400

($495)

$1,471

Chase Sapphire Preferred Yr 1

137,500

$0

$100

($95)

$1,380

Chase Sapphire Preferred Yr 2

37,500

$0

$100

($95)

$380

This shocked me; I was honestly surprised by how much better the Bilt cards were for booking repeated short stays than the Chase Sapphire Preferred card. First of all, the Chase Sapphire Preferred card is really good, and it currently has a huge 100,000-point sign-up bonus. However, even the Bilt Blue card outperforms it for the first two years, with the Bilt Blue card saving $2,245 and the Sapphire Preferred only saving $1,760.

The Bilt Obsidian and Palladium cards really show how well the Bilt program can work for repeated short stays. The Obsidian Card saves $2,855 over two years and the Palladium Card saves a whopping $3,567 over two years.

Scenerio 2 – $40K Annual Spend Example

Most travel sports parents will spend much more than $25,000 per year on things like groceries, gas, utilities, dining, etc. It’s expensive being a parent in general, but when you add in the cost of those basketball shoes or that bat they just had to have, let’s face it, you’re swiping that card more than that. Below is a more realistic example of $40,000 per year or a little above $3,300 per month. This still assumes a $1,000 per month spent on groceries, for the 3X points on groceries for the Bilt Obsidian card.

Card

Points Earned

Bilt Cash for Hotel Credit

Hotel Credit as Benefit

Annual Fee

Total Saved on Hotel Stays

Bilt Blue Yr 1

74,000

$450

$0

($0)

$1,375

Bilt Blue Yr 2

63,330

$900

$0

($0)

$1,691

Bilt Obsidian Yr 1

106,000

$450

$100

($95)

$1,780

Bilt Obsidian Yr 2

95,330

$900

$100

($95)

$2,186

Bilt Palladium Yr 1

153,330

$900

$400

($495)

$3,121

Bilt Palladium Yr 2

103,330

$900

$400

($495)

$2,096

Chase Sapphire Preferred Yr 1

160,000

$0

$100

($95)

$1,605

Chase Sapphire Preferred Yr 2

60,000

$0

$100

($95)

$605

In this example, the Bilt Blue starts to look way better than the Chase Sapphire Preferred. In two years the Chase Sapphire saves travel parents $2,210 on hotel stays while the Bilt Blue card saves $3,066 on hotel stays. This is crazy to me, since the Bilt Blue card was almost universally hated by critics when it came out and the Sapphire card is well regarded. Obviously, the reason why is the use of Bilt Cash for hotel credits.

What I was truly surprised by in this analysis was the Bilt Obsidian and Palladium cards. The Obsidian card saves the travel sports family $3,966 over two years, and the Palladium card saves $5,217 over two years! Typically in the points and miles space, you need to maximize multiple cards to get this kind of savings.

Scenario 3 – Supermarket Madness

There is a third method here for people who like to really maximize point earning. It occurred to me that by getting a Bilt Obsidian Card, choosing the 3x on grocery option, and spending $25,000 per year on groceries, you can maximize that card. This involves spending at least $333 at grocery stores on the first of the month, to earn double points up to a maximum of 1,000 bonus points and spending over $2,000 per month total at grocery stores. That sounds like a lot, but child athletes eat a lot, and groceries aren’t exactly cheap. Our family of four spends close to $15,000 a year, and we shop at Aldi. A larger family that shops at more traditional grocery stores should get close to that number. Also, keep in mind that many grocery stores also sell gift cards for things like Amazon or restaurants, if you want to extend those 3x categories to online shopping or dining. Any excess Bilt Cash, not used for hotel credit is used to unlock points earned by running housing payments through the Bilt ACH.

Card

Points Earned

Bilt Cash for Hotel Credit

Hotel Credit as Benefit

Annual Fee

Total Saved on Hotel Stays

Bilt Obsidian Yr 1

111,000

$450

$100

($95)

$1,842

Bilt Obsidian Yr 2

90,330

$900

$100

($95)

$2,146

In the above example, the Bilt Obsidian Card saves a total of $3,988 over two years. That beats the Bilt Obsidian card in the first example by $1,133 and the Bilt Palladium in Scenario #1 by $421. It also works out to an incredible 8% back on that spend. That sure beats a 1% or 2% cash back card. Also, since this example only uses grocery store spend, there’s really nothing stopping you from adding on the Chase Sapphire Preferred for additional points in other categories.

The Sweet Spot is Short Inexpensive Stays

A sweet spot is any unintended great deal in a loyalty program. My favorite example of this was when Turkish Airlines Miles and Smiles put together a partner award chart for Star Alliance flights. To keep things simple, they made all economy-class domestic flights 7,500 miles one-way. That’s a pretty good deal for Chicago to New York, but it’s an insanely good deal on a flight from New York to Honolulu. Unfortunately, that deal doesn’t exist anymore.

What Bilt wanted was to give people an incentive to book through their travel portal, where they earn a nice commission based on a percentage of the sale. That works great for them on expensive stays, but it’s probably not great for them when people book cheap hotels for short stays – the kind of thing you would book for a youth sports tournament. These types of stays are a sweet spot in the Bilt program.

It also doesn’t necessarily need to be just for sports travel. This also works well for couples who like to go on weekend getaways where a two-night stay is perfect. Regardless of why you stay in hotels, if you do it frequently and for short stays of at least two nights, using Bilt credit cards, and the Bilt Travel portal will save you a lot of money.

Coming off the recent devaluation of the World of Hyatt program and a change to the transfer ratio from Chase Ultimate Rewards to the World of Hyatt program, I think it’s time to ask a pointed question. Does it make sense to transfer points from any transferable points program to any hotel program?

In 2023, we stayed two nights at the Hyatt Ziva Los Cabos for a total of 43,000. For the same dates in 2027, it’s now 100,000 Hyatt points.

I’m not talking about situations where you need some points to top off your Marriott account to use the rest of your Marriott Bonvoy points on a hotel stay. I’m talking about situations where all of the points that you need to book a hotel stay are coming from a transferable points program. For the purposes of this discussion, let’s assume that the person booking the hotel never flies, since, generally, the best use of those points would be for airline tickets. In other words, they have points, and they are going to use them to book hotel rooms.

For each of these transferable programs, there is an option to use points on the travel portal to book a stay, rather than transferring those points to the hotel program and booking directly with the hotel.

American Express Membership Reward Points

According to The Points Guy, the value of an American Express Membership Rewards point is 2 cents. The chances of getting 2 cents per point value on a hotel stay using Amex points are extremely low, however. Amex has a laughably low redemption rate of 0.7 cents per point for hotels through their Amex travel portal. That becomes the baseline that you would have to beat to make a transfer make sense.

Program

Transfer From

Points Worth (TPC Valuations) in CPP

Transfer Value

Choice Privileges

Amex MR (1:1)

0.6

0.6

Hilton Honors

Amex MR (1:2)

0.35

0.7

Marriott Bonvoy

Amex MR (1:1)

0.8

0.8

In the case of Amex, I would probably transfer to Hilton or Marriott, simply because I would prefer to book with the hotel itself, because if something were to go wrong, you’d be better off having to deal with the hotel program itself, instead of dealing with the customer service from the Amex travel portal. But still, none of these options would even get you 1 cent per point. At these rates, if I’m not ever going to fly, I don’t think I’m even considering earning Amex points.

Bilt Rewards

Bilt Rewards is still a fairly new program, but they have grown to be, in my opinion, the best points program. One great aspect of the program is that, if you book a hotel through the Bilt Travel Portal, your points are redeemed at a 1.25 cents per point rate. In other words, a hotel that costs $125 per night would be bookable for 10,000 Bilt points. That is actually a really good rate by itself, but they also have six hotel transfer partners: All Accor, IHG Rewards, Hilton Honors, World of Hyatt, Marriott Bonvoy, and Wyndham.

Program

Transfer From

Points Worth (TPC Valuations) in CPP

Transfer Value

All Accor

Bilt (3:2)

2

1.5

IHG Rewards

Bilt (1:1)

0.55

0.55

Hilton Honors

Bilt (1:1)

0.35

0.35

World of Hyatt

Bilt (1:1)

1.55

1.55

Marriott Bonvoy

Bilt (1:1)

0.8

0.8

Wyndham

Bilt (1:1)

0.7

0.7

Of the six transfer partners, only two, All Accor and World of Hyatt, redeem at an average rate higher than the 1.25 cents per point that you can get through the travel portal. Points transferred to IHG, Hilton, Marriott, and Wyndham would essentially be burning those points, compared to just booking those hotels through the travel portal. The only good reason to transfer to one of those programs is to top off an account to use points that are already in one of those programs.

Capital One

Using Capital One Travel, Capital One Venture Miles are worth 1 cent per point when redeemed for hotels. Aside from booking on Capital One Travel, Venture Miles can be transferred to ALL Accor, Choice Privileges, I Prefer, and Wyndham.

Program

Transfer From

Points Worth (TPC Valuations) in CPP

Transfer Value

ALL Accor

Capital One (2:1)

2

1

Choice Privileges

Capital One (1:1)

0.6

0.6

I Prefer

Capital One (1:2)

0.5

1

Wyndham

Capital One (1:1)

0.7

0.7

All Accor and I Prefer end up with a value of 1 cent per point when transferring from Capital One Venture Miles. That’s the same value as booking through the travel portal, so it’s really just a matter of how you prefer to book the hotel. Wyndham and Choice provide very low value when transferring Venture Miles.

Citi Thank You Points

Citi Thank You Points are worth 1 cent per point for hotels through the Citi Travel Portal. Besides, what they are worth through the travel portal, Thank You Points can be transferred to several hotel programs. There are two different rates, but to get the highest transfer ratio, you will need to be a cardholder of either Citi Strata Premier or Citi Strata Elite. You can transfer if you are a cardholder of the Citi Custom Cash, Citi Strata, or Citi Double Cash, but the transfer ratios are so bad that I wouldn’t consider it. Below are the transfer rates if you hold a Strata Premier or Strata Elite card.

Program

Transfer From

Points Worth (TPC Valuations) in CPP

Transfer Value

Accor Live Limited

Citi Thank You (2:1)

2.0

1.0

Choice Privileges

Citi Thank You (2:3)

0.6

0.9

Leading Hotels of the World

Citi Thank You (5:1)

8

1.6

I Prefer

Citi Thank You (1:2)

0.5

1

Wyndham

Citi Thank You (1:1)

0.7

0.7

Actually with Citi, the transfer ratios are decent. With Accor and I Prefer, points transferred are worth a cent per point. With Leading Hotels of the World the value you get from a transferred Thank You point is 1.6 cents. That’s pretty good, unfortunately, it’s a small program with really expensive hotel rooms. If you want a really unique hotel stay, this is a good use of Citi Thank You Points.

Chase Ultimate Rewards

On the Chase Travel Portal, Chase Ultimate Rewards are worth 1 cent per point for hotels. On the portal, a points boost can yield up to 2x on hotels, however, that is up to Chase to determine what multiple you receive. For this discussion, we will assume no points boost.

Chase Ultimate Rewards has four transfer partners: Hyatt, IHG, Marriott Bonvoy, and Wyndham. Thanks to a new change in the Chase Sapphire Preferred, points are transferred at different rates depending on which card you hold.

Program

Transfer From

Points Worth (TPC Valuations) in CPP

Transfer Value

Wyndham

Chase Ultimate Rewards (1:1)

0.7

0.7

Marriott Bonvoy

Chase Ultimate Rewards (1:1)

0.8

0.8

IHG Rewards

Chase UR (1:1)

0.55

0.55

World of Hyatt

Chase UR w Sapphire Preferred (4:3)

1.55

1.16

World of Hyatt

Chase UR w/ Sapphire Reserve (1:1)

1.55

1.55

When transferring to Wyndham, Marriott Bonvoy, or IHG, you will get, on average, less than one cent per point. If you have the Sapphire Preferred, you will get slightly above 1 cent per point and with the Sapphire Reserve you will get over 1.5 cents per point, on average.

Always Check the Hotel Program First

The value of these points, with the exception of ALL Accor, are not set. Accor points are worth 2 Euro cents per point, meaning that a €200 per night hotel will always be 10,000 ALL Accor points. For the other hotel programs, the number of points per night to book a hotel could vary wildly. If you have a hotel in mind, check the hotel program’s website or app and see how many points they are charging. Then compare it with a travel portal and see which one will cost less in points.

Check for Transfer Bonuses

All of the math that I’ve included above does not include transfer bonuses. Hotel programs frequently offer transfer bonuses, that allow you to move points at a higher transfer rate and boost the value of your transferrable points. They change constantly, but a great resources is to use Frequent Miler’s Current Transfer Bonus page to quickly check for a transfer bonus before you book that hotel.

Where to Earn Points

If we ignore transfer partners for a second and assume you will only redeem your points through the travel portal for hotels, then it does become important where you earn them. At 0.7 cents per point for hotels through the American Express Travel Portal, I wouldn’t even bother earning Amex points for hotel stays. Capital One, Citibank, and Chase all offer redemptions at 1 cent per point, which isn’t too bad; however, Chase occasionally offers a points boost, and I would lean toward earning Chase points because of that. Bilt has them all beat with a redemption rate of 1.25 cents per point, so all things being equal, I would lean toward earning Bilt points when possible.

Conclusion

By default, I always lean toward transferring points to a hotel or airline program. I always assumed that I would get a better deal when doing it that way. Over time, I started to really narrow down that focus, and I found myself only looking at Hyatt properties when I was trying to transfer points from a transferable points program, because most other programs provided such weak value for those points.

Unfortunately, Hyatt appears to be hell-bent on devaluing their points, and since their changes to their award chart earlier this year, the value of Hyatt points has fallen from 1.7 cents per point to 1.55. I actually think it will continue to fall for the rest of this year, and then level off. To make matters worse, the transfer ratio from the popular Chase Sapphire Preferred card has fallen from 1:1 to 4:3. This makes these points barely better than going through the Chase Travel Portal.

Of the examples that I went through here, American Express Membership Rewards points are the worst for using on hotels. Their portal only gets 0.7 cents per point for hotels, and transferring points to their partners is a bad value as well.

Capital One, Citibank, and Chase all allow 1 cent per point redemptions on their travel portal, but other than a few examples, you can’t do much better than that. Capital One and Citibank get 1 cent per point to All Accor and I Prefer. Citi Thank You Points does better at 1.6 cents per point to Leading Hotels of the World, and Chase gets either 1.16 cents per point or 1.55 cents per point to Hyatt. Of those, Hyatt is the only one of those programs that isn’t pretty niche.

Bilt is slightly different. They offer 1.25 cents per point through their travel portal, and they only beat that with 1.5 cents per point to All Accor (again, pretty niche) and 1.55 cents per point to Hyatt. Bilt, in my opinion, is the clearly the best way to earn points for hotel programs, and if that’s your goal, I would earn as many Bilt points as possible.

At the end of the day, with only a few exceptions, you’ll do better booking through the transfer portals than transferring points. There is an advantage to booking directly through the hotel programs, in that if you do, it should be easier to deal with any issues that arise, since you will be dealing directly with that hotel program and not a third-party booking site. Also, not all programs will allow you to earn elite nights or use your elite benefits when you book through a third-party platform. If that is important to you, you may wish to use more points and transfer your points to the hotel program to book there.

But all things being equal, if you are someone who doesn’t stay enough in hotels to earn elite benefits or status and you just want the most economical way to book hotels using points, you’re probably better off booking through a travel portal. That is unfortunate, in my opinion. I would really like to see these banks work with hotel programs to boost the value of these points, because the value of transferrable points when transferring to hotel programs is laughably low.

On June 10th, 2026, Chase announced changes to the Chase Sapphire Preferred card that will go into effect on June 15th. Some of these changes were positive, improving earning rates on the card and increasing the value of the annual hotel credit. Unfortunately, one negative change could affect how people view Chase Ultimate Rewards and ultimately Chase Bank as a whole.

Chase Ultimate Rewards was the Standard

Chase has a special place in the hearts and minds of travel hackers. Starting in 2009, Chase launched the Chase Sapphire Preferred card, which introduced Ultimate Rewards points and allowed the transfer of those points to airline and hotel partners. Chase became a favorite because the earning rates on Chase Cards were lucrative and the transfer partners were great.

Before Chase Ultimate Rewards, Amex had Membership Rewards points. Later, Citibank introduced its own transferable points program, Citi Thank You Points, and Capital One created Venture Miles. Competition in the travel rewards space was fierce, but Chase kept one major advantage: 1-to-1 transfers to the most valuable hotel point program, World of Hyatt. It was such a strong partnership that people often referred to their Chase points as Hyatt points.

World of Hyatt Devalues and Transfer Ratio Changes

Earlier this year, Hyatt announced changes to its award chart that went from a 3-tier system to a 5-tier system. Essentially, each hotel now has 5 different prices they can charge in points for a stay, depending on the date. It allows the hotel more flexibility for what they can charge, in points, for award nights. On the surface, that seems reasonable, but the fear was that this would reduce the value of points because hotels would begin increasing the number of points required to book an award night.

These changes haven’t been in effect very long, but in the short amount of time it has been in effect, The Points Guy has dropped the value of Hyatt points from 1.7 cents per point to 1.55 cents per point, based on data collected from Gondola. It’s likely, in my opinion, that the value will continue to drop for a few more months before it levels off. How low it goes is really up to Hyatt at this point.

To complicate the issue with Hyatt’s devaluation, Chase has decided, with the new Sapphire Preferred changes, to change the transfer ratio from 1-to-1 to 4-to-3. What this means is that if you transferred 100,000 Chase Ultimate Rewards before the changes, you would end up with 100,000 Hyatt points. After the change, 100,000 Ultimate Reward points become 75,000 Hyatt points.

With the value of the points going down, what would have been $1,700 of Hyatt points (100,000 Hyatt points @ 1.7 cents per point) now is only $1,162.50 in Hyatt points (75,000 Hyatt points @ 1.55 cents per point). That’s basically like getting 1.16 cents per point on your Chase Ultimate Rewards points, which is barely better than just booking directly with the Chase Travel portal. If the value of Hyatt points falls further, there would be no reason to transfer at all.

Earning Rates Increase

One of the bright spots with the changes is that the earning rates in a couple of categories increased. The earnings at gas and EV charging stations rose from 1X to 3X. That can be significant if you spend a lot in those categories.

Another change is that you will now earn 3X on vacation rentals like VRBO and Airbnb. I really like this, because we prefer to stay in vacation rentals when we travel, and they can be a significant expense. Earning 3X would be a nice boost to our point totals.

Hotel Credit Increase

The Chase Sapphire Preferred Card had a $50 per year credit when booking a hotel through the Chase Travel Portal. Starting on June 15th, that credit will be $100. We’ve actually never used this credit, mainly because it was so small that we never considered using it. A $100 credit makes it something I might actually use, especially considering that you can combine the $100 credit with Ultimate Reward points at checkout. That means that a $200 hotel stay could be only 10,000 Ultimate Reward points after the credit, perhaps less if a points boost is attached.

Other Changes

Travel protections now include Emergency Evacuation and Transportation coverage. In addition, a $120, once every 4-year Global Entry, TSA PreCheck, or NEXUS credit has been added. A promotional complimentary 1-year Apple TV credit has been added as well. On the negative side, the 10% Anniversary Bonus benefit is being discontinued, which, frankly, never generated many points anyway.

Bottom Line

For me, this actually looks like a significant improvement. I think I might actually switch my gas charges to this card, as well as my Airbnb charges. I was using the Wyndham Business Earner card for 8X on gas, but I’m just not seeing tremendous uses for Wyndham points, so I think I’d rather earn Ultimate Reward points.

The change in the hotel credit from $50 to $100 means that I might actually use it. We’ve held at least one Sapphire Preferred card for years, and we’ve never actually used the credit. Knowing that I can use the credit for a short stay, especially if it’s a one-night hotel stay on a positioning flight or on a road trip, makes this extremely worthwhile.

Where this hurts is for people who racked up a ton of Chase Ultimate Reward points, transferred all of them to Hyatt, and redeemed those points for high-end hotels and all-inclusive resorts. This almost forces those people to pay the $795 annual fee for the Chase Sapphire Reserve, because that card maintains a 1-to-1 transfer ratio to Hyatt. Unfortunately, even that doesn’t guarantee that Hyatt points won’t continue to devalue.

In the end, I think a lot of people will look at this and think that maybe they’re better off focusing on other hotel programs. If you were someone who put significant spending on Chase cards to earn points to transfer to Hyatt, you might give up on Chase altogether, after all, it’s not clear what the value of Hyatt points will be in 6 months to a year.

For people who love Hyatt, they might choose, instead, to get a Bilt card. Bilt still transfers its points 1-to-1 to Hyatt. Depending on which card they get and what categories they spend their money in, people might be better off earning points in Bilt and transferring to Hyatt.

All in all, while the changes to the Chase Sapphire Preferred will work better for me, I think it’s a significant risk that Chase is taking. The transfer partnership with Hyatt was a major selling point for Chase, and now, it just looks rather ordinary. For those people who loved the Hyatt program and its relationship with Chase, this is a huge disappointment and is likely to change the spending behavior of those Chase customers.

For the first time in about four years, we aren’t doing any traveling, and we’re not really planning any trips either. It’s a bit of a strange feeling. I’ve been at least partially focused on travel for a long time, but it’s just not important right now. Instead, we have been helping our daughter look for a house, and our son look for a college. In addition, I’ve been working on a house project that has been taking way more time than it should.

That being said, it’s not lost on us that once Alex leaves for college and Emma moves out of the house, Jenn and I will have more freedom to travel, because we won’t have to work around their schedules nearly as much. That means that right now, we should be accumulating and hoarding points while our lives are not focused on traveling.

Next summer, we will be taking Alex’s graduation trip. We did this for Emma when she graduated, and while she didn’t really plan the trip, we did allow her to guide where we went. Alex has suggested Iceland and Finland, and frankly, it’s likely to be Iceland OR Finland, with some time in Southern Europe, depending on what works with points. Finland and Iceland aren’t exactly cheap, so 10 or so days in hotels or Airbnbs in Northern Europe could get pretty expensive, not to mention the cost of food. Spending some time in Southern Europe could really cut down on the price of food and lodging.

Programs to Focus On

When thinking of traveling to Europe, I normally think of a few programs. In the few trips we’ve made to Europe, we’ve used Aer Lingus, Iberia, and British Airways with Avios, as well as KLM using Flying Blue miles. We’ve also used American Airlines AAdvantage, United Miles, and Delta Skymiles. In addition, we’ve flown on United using Singapore Airlines miles and SAS using Avianca Lifemiles. Basically, I’ll use anything if it makes sense.

The thing is, when I look at our points totals, I see a lot of programs without a ton of points in any specific program. Considering where we currently have the most points, it probably makes sense to beef up point totals where we already have a decent number of points to make sure that we have enough points to book everyone at the same time.

One choice is to book with Aer Lingus, Iberia, or British Airways with Avios. We only have a little over 80,000 points. That can be bumped up with our Amex Membership Rewards points, Chase Membership Rewards Points, Citi Thank You points, Bilt Points, or Capital One Venture Miles. We’ve had good luck with American Airlines, so earning American Airlines miles would be great, but we can only transfer from Citi Thank You points. United might also work, and we can transfer from Chase or Bilt to add to our United points total. Alaska Airlines Atmos miles has some inexpensive partner awards to Europe, but they only transfer from Bilt.

Because we would most likely be using Avios miles, Atmos miles, AAdvantage Miles, or United Miles, it makes sense to try our best to gain miles with signup bonuses that are either with one of those airlines or with Bilt, Chase, or Citi Thank You. Bilt doesn’t have many good opportunities to earn signup bonuses, so focusing on Chase or Citi makes sense.

In reality, my plan is to try to jump on any elevated signup bonuses that align with these programs. Unfortunately, right now, I’m not seeing anything that seems to be elevated, so I’m waiting for something to change. I can’t be patient forever, though. Right now, we aren’t working on a signup bonus on anything, and that does feel a little like we’re wasting time, so the longer we wait, the less patient I’ll probably be.

Schrodinger’s Wyndham Points

Jenn’s Wyndham Business Earner card has renewed again, which essentially means that we got 15,000 Wyndham points in exchange for paying the $95 annual fee. 15,000 Wyndham points are worth around $105, so that’s not terrible, but with Wyndham not partnering with Vacasa anymore, I’m not nearly as excited to use those points. It’s possible to book a Wyndham Vacation Club stay with points, but the availability is greatly limited, and the locations don’t thrill me.

Most likely, we will try to use Wyndham points on one of their all-inclusive properties, which look okay, but not spectacular. Typically, at all-inclusives, we just want to hang out at the beach and the pool and have a few drinks, so they’ll probably be fine for us. We’re going to have to book one and find out. Until we try out their all-inclusive resorts, I won’t have any idea whether we want Wyndham points going forward.

On to the Points Check

We earned a whopping 9.2% back on our spending not devoted to a signup bonus. Some of that was due to a 3,000 Membership Rewards Points bonus that was an Amex offer on my Amex Green card, which said that we would earn 1,000 points for a $40 order with Amazon. We needed to order something that was $150, and shockingly, they gave us 3,000 points. Apparently, I didn’t read the offer properly because they seemed to give me 1,000 points for each $40, and I’m not sure what the maximum was.

Card Used

Spend

Points Earned

Point Value

Points Per $

Return on Spend

Ink Cash

$744

3,724

$76.34

5.0

10.3%

Bilt Palladium

$483

2,477

$54.49

5.1

11.3%

Custom Cash

$481

2,338

$44.42

4.9

9.2%

Wyndham Business Earner

$396

1,981

$13.87

5.0

3.3%

Amex Gold

$311

475

$9.50

1.5

3.1%

Blue Business Plus

$186

372

$7.44

2.0

4.0%

Ink Unlimited

$183

275

$5.50

1.5

3.0%

Amex Green

$150

3,150

$63

21.0

42.0%

Chase Sapphire

$146

438

$9.45

3.0

6.2%

Total

$3,080

15,230

$283.54

4.9

9.2%

This month’s spending not devoted to earning a signup bonus

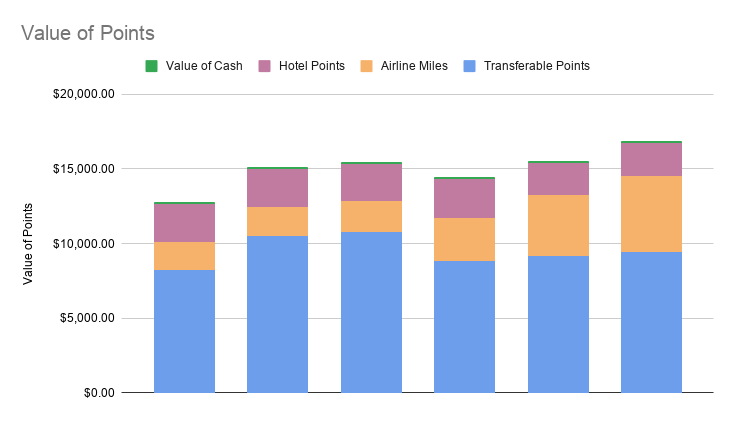

Besides the money spent on the above cards, Jenn spent a little over $2,700 on her Atmos Ascent card and earned a little less than 2,800 Atmos points. She also completed the required spend to collect the 70,000 Atmos point bonus on that card. That leaves us with:

260,300 Chase Ultimate Rewards Points

230,400 IHG Points

156,600 Alaska/Hawaiian Airlines Atmos Miles

121,700 Wyndham Points

93,800 Amex Membership Rewards Points

92,600 American Airlines Miles

81,800 Avios

75,200 Bilt Points

24,700 Citi Thank You Points

19,300 United Miles

15,900 Marriott Bonvoy Points

1,500 Delta Miles

300 Hyatt Points

$133 Cash Back

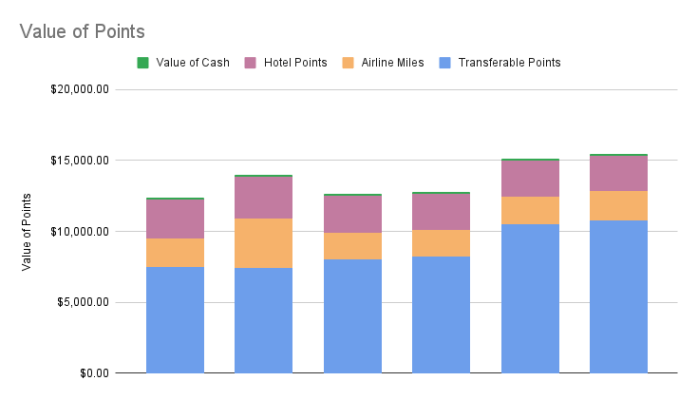

According to the valuations published by The Points Guy, these points are worth a total of just under $16,800. That is an all-time high for us. Without any plans coming up, I expect that we should be able to pad these numbers for a few months, until we need to start booking Alex’s graduation trip. Until then, I have a project to finish and a kid to get to some college visits.

March in the Midwest can be frustrating. The winter is long, and we all begin to hope that winter is officially over. A couple of warm days early in the month marked what we call “False Spring” which raised our hopes. This was, of course, followed by an ill-timed blizzard which affected our Spring Break trip to Tenerife.

We saw the blizzard forming in the weather forecast for a week or so prior to the flight and ended up making some not ideal decisions with our points to save the vacation. Making these changes was more difficult than it should have been and cost us quite a few points. In retrospect, maybe I would have done things differently, but those last-minute decisions meant that we were able to save the vacation.

On the trip, itself, we explored London for a couple of days, then Tenerife for five days, and Madrid for one day. I wasn’t excited about London, but we had a great time, and I hope we get a chance to have another stopover there and explore other neighborhoods, since it’s such a large and diverse metropolitan area.

Palace of Westminster

This was also our second stop in Madrid, and we didn’t enjoy it the first time, but this time it was great. Madrid, like London, is huge, and it’s really important to choose your neighborhood carefully. The first time, we stayed in Salamanca, an upscale part of Madrid, which wasn’t really our thing. This time we stayed near Plaza Mayor in Centro, and it was fantastic. The energy of the city, the crowds of pedestrians, and the amazing food scene all combined to make for an exciting stay in Madrid. Now I understand why people love Madrid so much.

Plaza Mayor Madrid

What Those Flight Changes Cost Us

In order to avoid our flight being canceled and us missing at least the beginning of the trip, we canceled our American Airlines flight to London and received 19,000 AAdvantage miles each back, for a total of 57,000. Emma had her own miles, and she got her 19,000 AAdvantage miles returned to her account as well. Unfortunately for us, we had to book her on the United flight we took, because she wasn’t able to.

We used 65,000 American Express Membership Rewards points transferred to Singapore to book the two flights for Emma and Jenn, and 76,000 Chase Ultimate Reward Points to transfer to United to book the flights for Alex and me. 57,000 American Airlines miles back definitely does not make up for those transfers, but at least we were able to make the trip, and the flight arrived 5 hours earlier than the American flight would have arrived, so we got more time in London. Emma was the big winner, though, getting all her points back without having to use any other miles.

Bilt Palladium Bonus

Jenn completed the spending necessary to earn the signup bonus on her Bilt Palladium Card. This card will be our go-to card for most things going forward, when not working on a signup bonus. Because we are able to essentially earn 4x on the first of the month, 2x the rest of the month, with an additional 1x with the points accelerator and an additional 1x when running our mortgage through their ACH processor, we will probably earn around 3X on everything when we are using that card. Since those points transfer now to an eye-popping 25 transfer partners, it won’t be difficult to find good uses for those points.

Bilt Tax Payment Blunder

We’ve used tax payments in the past to help us quickly earn a signup bonus. Typically, the math doesn’t work out when paying your taxes by credit card, because you would earn 1X on most cards while paying around a 2% fee. Some cards earn 2X, which means that you would essentially be earning 1 point for every cent you paid for the processing fee. That’s not terrible, and depending on the type of points, you might want to do that.

My daughter had about a $1,000 to pay to Uncle Sam, and we said we’d process it on our Bilt card, thinking that we would get the 2X on all charges, plus the 1X on the points accelerator, as well as move us closer to getting the signup bonus. Unfortunately, I didn’t read the fine print, because tax payments aren’t eligible to earn points, and it doesn’t count toward the signup bonus either. Essentially, because I wasn’t paying attention to the details, we paid 2% on the transaction and got absolutely nothing for it. Not great – don’t use your Bilt Card for tax payments!

On to the Points Check!

Most of the spending not devoted to signup bonuses was recurring payments, except for what we spent on Jenn’s Amex Gold card. That card has become the default for our son, who is an authorized user, to use when we need him to pick something up for us or when he needs something. I don’t imagine all of that is from him, but the fact that we only earned 1.4 points per $ spent on that means it wasn’t being used on groceries or dining very much (where it earns 4x).

Card Used

Spend

Points Earned

Point Value

Points Per $

Return on Spend

Amex Gold

$653

898

$17.96

1.4

2.8%

Wyndham Business Earner

$353

1,764

$19.40

5.0

5.5%

Ink Cash

$344

1,719

$35.24

5.0

10.3%

Blue Business Plus

$68

136

$2.72

2.0

4.0%

Total

$1,418

4,517

$75.32

3.2

5.3%

This month’s spending not devoted to earning a signup bonus

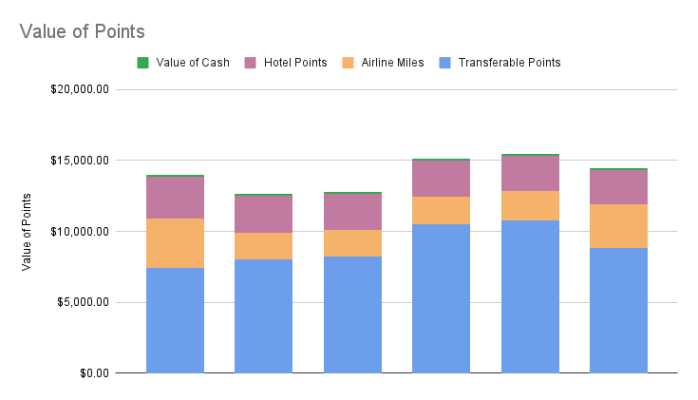

Aside from the spend not devoted to signup bonuses, I spent a little less than $1,900 on my Iberia Visa Signature card, earning a little over 2,000 Avios. Jenn spent a little over $4,000 on her Bilt Palladium Card and earned over 9,700 Bilt points as well as the 50,000-point signup bonus. Overall, our spending was pretty high, but not surprising with a trip and our daughter’s tax payment thrown in there.

All of this left us with:

252,800 Chase Ultimate Reward Points

229,900 IHG Points

102,900 Wyndham Points

88,900 Amex Membership Rewards Points

92,600 American Airlines Miles

79,400 Alaska Miles

64,300 Bilt Points

19,700 Citi Thank You Points

16,700 United Miles

15,900 Marriott Bonvoy Points

3,600 Avios

1,500 Delta Miles

300 Hyatt Points

$133 Cash Back

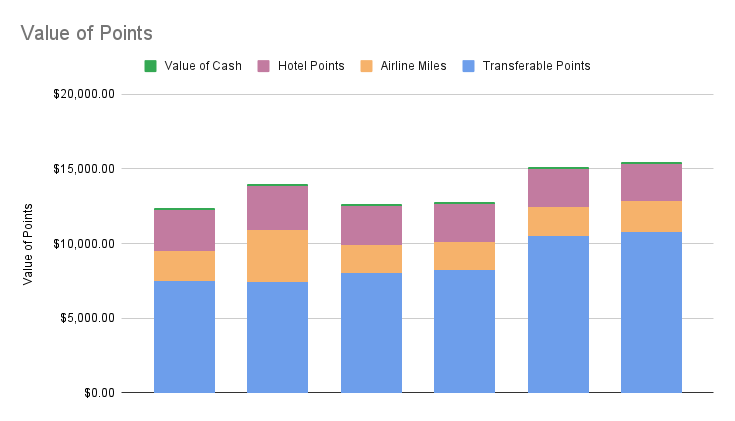

According to the valuations by The Points Guy, the total value of points and miles is $13,000. This is a significant drop from the $15,300 last month and is almost exclusively because we had to change our travel plans at the last minute, and that’s even after getting a bonus from Bilt. I had planned to be a little less aggressive this year with signup bonuses, but with a big trip planned for next summer, that may not be an option. We’re going to have to get some points banked in order to do what we have planned.

We’d had this trip planned for months. A sunny few days in Tenerife with a two-day stop in London at the beginning and a one-day stop in Madrid at the end.

The long-haul flights from Moline to London and Madrid to Moline were on American Airlines and booked with AA miles. We got a tremendous deal on the flights from Moline to London for 19,000 AA miles and $5.60 each, for four people. The flight home was a good but not great price, costing 34,000 AAdvantage Miles and $50 each. We also booked award flights on British Airways from London to Tenerife and Tenerife to Madrid on Iberia Airlines.

Everything looked great, and we were ready to go, but a couple of months prior, American Airlines had moved the first leg of our flight to London forward two hours which meant that the comfortable 3 hour layover in Chicago was now a nerve racking hour and seven minute layover.

Jenn and I considered moving our first leg of the flight to an earlier flight, but that would have left us with a six hour layover in Chicago and we thought “you know, let’s just trust the airline this time, as long as the weather is fine, that’s an easy enough connection.”

The Weather Was, in Fact, Not Fine

We live in the Midwest. We know better. There is no such thing as “fine” weather, especially in March. It’s 5 degrees one day, 70 degrees the next. It’s also constantly rainy, windy, and occasionally, we get the dreaded March blizzard.

About a week before our trip, our local meteorologist started talking about a storm coming up. He was predicting strong winds and maybe an inch of snow. As the week progressed, the forecast progressively got worse, and we were looking at the prospect of attempting to fly out of our local airport with sideways snow accumulating in the 5 to 8 inch range.

Moline does not have a great reputation for on-time flights, so our 1-hour layover now looked impossible. We needed options. What I was hoping for was either a longer layover or a different route that got us around the storm. I searched every way I could think of and couldn’t come up with a good alternative.

I took about a day to try to figure something out and the forecast kept getting worse, so we finally thought “what if we drove to Chicago the day before and just took the Moline to Chicago legs off of our flights?” That way, no matter what, we wouldn’t miss the flight from Chicago to London. Sounds great, but we’ll have to call American Airlines to do that.

We called and they answered the phone almost immediately. We explained the situation to the customer service representative. She responded that she could rebook us from Chicago to London, and that would cost 30,000 points.

Wait – what? I’m going to give you 4 seats back, that you can sell, or potentially use for other passengers who might be impacted by the storm, and you want me to pay an additional 11,000 AAdvantage miles per person to do it?

I barely had enough points to do it, but that also means that I would have to change our flights back since my truck would be in Chicago, and we definitely didn’t have enough AAdvantage miles to change both. I knew we could skiplag on the way home and just get off in Chicago, but it’s frowned upon, and I didn’t want to piss off American Airlines.

We talked about it and decided that, since we were willing to drive to Chicago, we should look into whether we could get flights from Chicago to London on United Airlines. Jenn checked the United app and saw that saver-level fares were available for a little over 38,000 United miles. That’s great, but I knew if there were saver-level fares available on United, then they might be available on Singapore Airlines as a partner award. I preferred to use Singapore Airlines to book, because they generally have cheaper prices on United flights to Europe and they have a lot of transfer partners.

The Singapore Airlines Nominee Problem

I checked the Singapore Airlines website and, sure enough, there were the same flights available for only 32,500 Singapore Miles instead of 38,000 United miles. Great – we then transferred 130,000 miles from American Express Membership Rewards to Singapore to book the flights. I then tried to book the flights and ran into a problem. It was Jenn’s Singapore Airlines account, and I could add Emma and Jenn, but there wasn’t any way to add me and Alex.

It was strange. Why could I only choose from a dropdown instead of just filling out the passenger information? Jenn called customer service, and they said that we needed to add “nominees” (Emma was already a nominee for Jenn’s account because they booked a trip together last summer using Singapore). Ok, fine, it’s weird they do it that way, but sure. Jenn added Alex and me to the nominees and then tried again to book it. She still couldn’t choose us. Jenn called back to customer service, and they told her that she couldn’t add nominees for flights within 72 hours – we were looking at a flight 52 hours in the future. You’ve got to be kidding me.

At this point, I was getting pretty frustrated, but we decided to book Emma and Jenn using Singapore Airlines, since we had already transferred the points, and Alex and I would have to book the same flights using United miles.

The United Mileage Pool Problem

We’ve had around 13,000 United miles in a family pool for a while now. We needed a total of 76,000 miles to book Alex and me on the same flight to London that Jenn and Emma were now on. So I transferred 63,000 Chase Ultimate Reward points to United and then added them to the family pool.

Now I just needed to book the flight. I chose the flight and then went to check out and got the error “You do not have enough miles to book this flight.” What? Why? I poked around for a while, and it said that pooled miles were not available for this flight. I’m sorry, what? No explanation as to why, just that I couldn’t use the miles for this flight, and a link to the terms and conditions so I could sift through all of the carefully written legal language for the rule that applied in this case.

I was at the end of my rope; I just needed to get this flight booked. I was frustrated because I had moved points over to the family pool, and I wasn’t sure if I could get them out of the pool to use them immediately, and I had already stranded 65,000 Amex Ultimate Reward points on Singapore Airlines since Alex and I weren’t nominees on Jenn’s account.

I did some searching and found out that I could reverse a move to a points pool within 24 hours, so I reversed the move and transferred an additional 13,000 Chase Ultimate Reward Points to United, which gave me enough points outside of the points pool to book the flight.

Frustrations with Loyalty Programs

At the end of all of this, I was frustrated, angry, and frankly disappointed in each of these loyalty programs. Every problem I experienced trying to fix a problem with the weather was created by an unnecessary rule. For most of these, I don’t even understand why the rule exists in the first place, let alone why you would put your customers (and customer service representatives) through this.

American Airlines – Dynamic Pricing Demands More Flexible Customer Service

For American Airlines, you put out a travel alert for our flight. You knew the weather was going to be bad. When we explained to the customer service representative what we were attempting to do and why, she completely understood. She talked to her supervisor to explain the situation, but still couldn’t do anything about it without having to rebook.

If you are going to have dynamic pricing, then you cannot expect people to rebook at higher prices later if there is a weather emergency. It would be one thing if we decided that we wanted to change our flights and there were no weather issues, but that wasn’t the case. You declared a travel alert, but then were too narrow in what we could do to address the weather issues. And we weren’t even trying to get on a flight that we hadn’t booked – we just didn’t want to take one of the legs of the flight. We couldn’t have made it easier on you. They still couldn’t accommodate the simplest of requests.

Singapore Airlines – The Nominee System is Terrible

For Singapore Airlines, what are you doing with this nominee system? This is utterly insane. I understand that you are probably trying to prevent people from selling your points, but if the account holder is literally flying on the same flight, then they’re not selling points, they’re just trying to get their family or friends on the same flight that they are on.

The nominee system is a complete waste of your IT staff and your customer service staff’s time. Just allow people to type in the information of the people who will be on the flight, like everyone else does. Also, if you are going to force a nominee system, then why in the world would you not allow someone to book within 72 hours? It makes no sense, and this is just an unnecessary rule that you are forcing your customer service representatives to know, explain, and enforce, while undoubtedly pissing off your customers.

United Airlines – Make Points Pooling Instantaneous

For United Airlines, can you make the points pooling useful? Making me wait 24 hours after pooling points is asinine. Like American Airlines, you use dynamic pricing, so if I move a certain number of points over to the points pool, there is no guarantee the price of that flight will be the same the next day. What if I move enough points over today and the price jumps by 5,000 points tomorrow, and then I move another 5,000 points, and then it changes the next day? You can’t have dynamic pricing and not allow me to use points immediately; that’s just going to lead to frustration, anger, and uncomfortable phone calls for your employees.

In addition, it would be nice if you could explain why I couldn’t use pooled points on a flight in the error and maybe tell me what I could do about it instead of just linking the terms and conditions. I literally didn’t know why I wasn’t able to book that flight until a week later when I had the time to really look into it.

We Saved the Trip

At the end of the day, we were able to make it work. The original flight from Moline to Chicago that we were trying to avoid got canceled, so had we not changed our plans, we would have been at the mercy of American Airlines to get us to London, at best, a day late. The issue with Singapore Airlines meant that we had 65,000 Amex Membership Rewards points stranded there, and the clock is ticking, since they now expire in 3 years.

I tried to rebook the flight from Madrid to Moline to Madrid to Chicago, but there weren’t really any available seats anywhere to make that work. We ended up having to skiplag the Chicago to Moline portion because, as we found out, there is no point in calling American Airlines customer service to let them know we won’t be using the last leg. I hated doing that, but we really had no options.

On the bright side, we landed in London about 4 hours earlier than we would have on the American Airlines flight, and every other part of the trip was the same. Having points in multiple programs allowed us to move around what we needed to and book a workable flight. As frustrating as all of this was, it was less frustrating than being stuck because of the snowstorm and missing out on a portion, or all, of our vacation. I’ve heard this many times, and it turned out to be true – always be proactive when you are traveling, and make sure that you stay out in front of any issues, especially weather problems.

February in Iowa is brutal. It’s been cold and dark. Midwestern winters are primarily about survival. You just go inside and stay. Most people binge-watch TV shows under a heated blanket. We’re not big television watchers, so we’ve been spending an unhealthy amount of time in breweries, where the Quad Cities excels in both quantity and quality. Illnesses are running rampant, as Iowans have been breathing the same indoor stale air since November. At this point, we’re all just dreaming of going outside for anything.

Because of all of this, if you go anywhere to Florida, Arizona, or the Caribbean during March or April, you will run into dozens of folks from the Midwest, in our annual desperate attempt to bookend the hellscape that is Midwestern winter. Spring break isn’t an annual tradition; it is the only thing that keeps us from tying a brick to our legs and jumping into an icy lake in the winter. WE NEED THIS!

For the last three years, we’ve planned unusual Spring Breaks. Frankly, we’ve done Florida, and I just can’t do it anymore. I don’t want to share a beach with obnoxious, drunken college students. Because of that, our Spring Breaks have been a little different lately. Two years ago, we went to Costa Rica and spent time hiking in the mountains, lying on the beach, and enjoying Costa Rican culture. Last year, we spent six days hiking the Portuguese route of the Camino de Santiago. This year, we will visit the Canary Islands, specifically Tenerife Island, which is part of Spain, but off the coast of Africa. This will give us a beach vacation, but without the crowds of Florida and the Caribbean. We will also be stopping in London and Madrid as part of this trip.

Spring Break couldn’t come soon enough, because we are starting to lose our minds here, and it’s time for us to go outside and get some vitamin D.

Atmos Awards Ascent Visa Card

We said we weren’t going to do this. We were going to take it easy and sign up for fewer cards this year, but alas, Jenn signed up for the Atmos Awards Ascent Visa Signature card. This is while I’m working on a signup bonus for my Iberia Plus card, and Jenn is working on a signup bonus on her Bilt Palladium Card.

There was a valid reason for this: Jenn wants to plan a girls’ trip with her and Emma to celebrate Emma turning 21 and is considering options in the Northwest, including Seattle, San Francisco, or Portland. Atmos miles would work really well for any of those destinations, and now that she earns Bilt points, she has a way to top off the account by transferring Bilt points to Atmos. It’s always a good idea to pair a hotel or airline card with a transferable points card to have some flexibility and top off an account. Having the Bilt card makes the Atmos card more attractive.

The Atmos Awards Ascent Visa Card has a $95 annual fee and earns 3X on Alaska Airlines purchases, 2X on Gas, EV charging, transit, rideshare, cable, and streaming services, and 1X on all other purchases. If you spend $6,000 in a year, you will earn the companion fare, which allows you to book a companion flight for $99 plus taxes.

The current bonus for this card is 70,000 points when the cardholder spends $4,000 over the first 90 days. The Atmos Awards program is known for strong partner booking rates. Short-haul domestic flights on American Airlines typically cost 4,500 points, and I see many routes to Europe for 27,500 points with minimal fuel surcharges. Having a few more Atmos miles will be a good thing to have around.

UK Electronic Travel Authorization

Since 2025, the UK has required an electronic travel authorization to enter the UK from the United States. This is to enhance their border protection. Each application costs 16 British pounds and, if approved, is good for two years. On their website, they say to allow up to three business days to process the application, so you need to plan ahead.

This will be our first trip to England, and while I’m not happy about the fact that I have to pay for four authorizations costing a total of $90, we went through the process and found it to be fairly easy. We used the phone app to apply, and I think that might be the reason. Using an iPhone, it was able to scan our faces, scan our passports, and take photos of us and our passports. Scanning the passport was interesting; apparently, there is a chip in the back cover of your passport, and it was able to read it through the phone.

Anyway, this process took just a few minutes, and we were approved immediately. There is an option to apply online, and I assume that you would not be able to scan the passport or your face, and maybe when you apply that way it takes them longer to verify the information. That might be why we were approved instantaneously and they say to allow three business days. So if you do have an emergency trip to the UK, I would use the app, I think that will give you a better chance of instantaneous approval.

On to the Points Check

We spent around $2,500 on cards not earning a bonus, earning less than 5% return on that spend. That’s below where I want to be. I want to shift as much of this to the Bilt Palladium card over time, since that has solid earnings on all spend. I’m going to continue to keep utilities on the Wyndham Business Earner card since it earns 5X on utilities, and I’ll keep our phone bill and streaming services on the Ink Cash since it earns 5X on that spending. But other than that, most of this would be better spent on the Bilt Palladium Card.

Card Used

Spend

Points Earned

Point Value

Points Per $

Return on Spend

Amex Gold

$1,333

2,619

$52.38

2.0

3.9%

Sapphire Preferred

$508

772

$15.83

1.5

3.1%

Ink Cash

$441

2,204

$45.18

5.0

10.3%

Ink Unlimited

$101

153

$3.01

1.5

3.0%

Wyndham Business Earner

$84

420

$4.62

5.0

5.5%

Blue Business Plus

$66

132

$2.64

2.0

4.0%

Total

$2,533

6,300

$123.71

2.5

4.9%

This month’s spending not devoted to earning a signup bonus

Aside from the spending above, I spent a little over $1,600 on my Iberia Plus card, earning 1,600 Avios, and Jenn spent a little over $1,600 on her Bilt Palladium card, earning almost 4,600 Bilt Points. We used $200 in Bilt Cash to activate the Points Accelerator, which adds an additional 1 point per dollar spent on the next $5,000 in spend. That essentially makes the Palladium Card a 3X anywhere card.

That leaves us with a total of:

327,000 Chase Ultimate Reward Points

247,300 IHG Points

175,800 Amex Membership Rewards Points

101,200 Wyndham Points

79,400 Alaska Miles

33,900 American Airlines Miles

19,300 Citi Thank You Points

16,700 United Miles

15,900 Marriott Bonvoy Points

4,600 Bilt Points

1,600 Avios

1,500 Delta Miles

300 Hyatt Points

$133 Cash Back

All of this, using the points valuations published by The Points Guy, is worth a total of $15,300. That’s the highest it’s been in a while, which is great, but right now I’m a little more focused on getting out of this winter hellscape and getting to a beach. I can’t wait to get to Tenerife.

On January 14th, 2026, Bilt released the details on the three credit cards that were replacing the original Bilt credit card. The original Bilt card was issued by Wells Fargo and it was widely reported that it was a significant money loser for them. These three new cards are issued by Cardless, and are intended to be a profitable way for the Bilt Program to issue credit cards.

The Five Banana Problem

The original Bilt credit card allowed users to earn one point per dollar when putting their rent on the credit card as long as they used their card five other times per month. The intention was that Bilt would recoup the money lost from interchange fees (which landlords don’t pay but retailers do) by generating it back through interchange fees from other purchases. The problem was that many savvy users swiped the card for five small purchases each month (such as a single banana), which didn’t generate much revenue for Bilt. Therefore, the joke was that Bilt had a five-banana problem.

With the new credit cards, Bilt believes they have solved the five-banana problem by creating a second currency called Bilt Cash that is earned each time the user swipes the card on non-rent or mortgage purchases. That Bilt Cash can be used to unlock the points earned from rent or mortgage payments. It’s strangely complicated, but the short answer is that if you spend 75% of your mortgage payment on other things, you earn enough Bilt Cash to unlock your points. In other words, to get the 1,000 points earned from a $1,000 mortgage payment, you would need to use it for $750 worth of other spending. Five banana purchases won’t work anymore.

What is the Bilt Blue Card?

The Bilt Blue Card is a no-annual-fee credit card that earns 1X on all spend and 4X Bilt Cash on all purchases (mortgage and rent payments are not made on the card itself). It also earns 1X on all rent or mortgage payments, but requires 3% of the total transaction in Bilt Cash to unlock those points. In other words, you need $30 in Bilt Cash to unlock the points from a $1,000 mortgage or rent payment, and at the 4x rate to earn those points, you would earn $30 in Bilt Cash after $750 in purchases.

Technically, the 1X earned on housing spend is not on the credit card, since that is not allowed. The housing payments must be done by ACH or Venmo using the Bilt website. The old card allowed you to charge the rent to the card itself, and this change appears to be an effort to reduce costs and make the Bilt card profitable.

Yes – I get it – this is complicated, but the point is that you can earn valuable Bilt Points on your rent or mortgage as long as you are actively using that credit card for a significant amount of your monthly spend. This is unique because you cannot do this to earn Chase Ultimate Reward Points, Citi Thank You Points, Amex Membership Reward Points, or Capital One Venture Miles.

Transfer Partners

What is also unique about the Bilt Blue Card is that it is a no-annual fee that allows you to earn points that can be transferred to airline and hotel programs. Transfer programs are what really make Bilt Points valuable, and while Citi, Chase, Amex, and Capital One have transfer partners as well, most require a credit card with an annual fee to unlock the ability to transfer.

In addition, Bilt points are the most valuable of any of the major transferable currencies. That is because they have a ton of transfer partners, and some of the most coveted. On the airline side, Atmos rewards is a highly valued currency for its ability to book partner awards for not a lot of points. On the hotel side, you can transfer to Hyatt, whose points are extremely valuable. The complete list of transfer partners, as of January 2026 are:

Aer Lingus (1:1)

Air Canada (1:1)

Atmos Rewards (Hawaiian Airlines and Alaska Airlines) (1:1)

Avianca Lifemiles (1:1)

British Airways (1:1)

Cathay Pacific (1:1)

Emirates (1:1)

Etihad Guest (1:1)

Flying Blue (KLM and Air France) (1:1)

Iberia (1:1)

Japan Airlines (1:1)