January was the start of a pretty big year for us. Just two years ago, I was in the middle of planning our first trip to Europe. I honestly couldn’t believe that we were going, it had been a dream of mine my entire life and then finally, in my late 40’s I was getting a chance to go. And then, last year we got a chance to go to Europe for a second time.

This year, however, we have plans to go to Europe three times, and that just seems crazy to me. In March, the four of us will be heading to Portugal and Spain so we can hike the last 120 kilometers from Tui to Santiago de Compostela on the Portuguese route of the Camino de Santiago.

In September, Jenn and I will be going to Nice, France for the UTMB Cote d’Azur Ultramarathons, where I will be doing a 54 kilometer race and Jenn will be doing the 22 kilometer version. Our friends Bill and Theresa will be joining us and also doing the 22 kilometer race. After going to Nice, we will end up for a couple days in Dublin before heading home.

The summer trip, is a little unsettled at this point. It’s not booked, but Jenn and Emma will be going to Europe with Jenn’s sister and our niece, who will be graduating from high school this year. The tentative plans are to go to Munich for a few days, then to Dublin and head home.

This leaves our son Alex and I with nothing to do, so I’m hoping we can find an excuse to go to Europe around the same time, maybe for a hiking trip. I’m eyeballing the Alps, or the Malerweg near Dresden, Germany or perhaps even Madeira, Portugal. I’m going to wait until after our trip to Spain to see how much we feel like hiking. It might be up to what flight deals are available to determine where we are going.

Taking Alex to His First Concert

Alex’s favorite band had a concert in a small venue in the West Loop of Chicago. He asked if he could go and we decided to buy him and our daughter, Emma tickets and told Emma that she needed to take him, since she is 19 and he was about to turn 16.

As the concert got closer, we started thinking “Are we really going to let them go to Chicago on their own and stay the night in a hotel there?” We eventually decided that we would drive them to Chicago and book separate hotel rooms, that way they could at least pretend to be somewhat independent and we could enjoy a night away.

We stayed at the Hyatt House West Loop – Fulton Market and we used a free night certificate from my World of Hyatt personal card for one room and 12,000 Hyatt points transferred from Chase Ultimate Rewards for the other. Those rooms typically cost around $180 per night so we got about 1.5 cents per point value on the redemptions, which is a little low for Hyatt points, but I really liked the hotel. The rooms were very large, modern and comfortable. They also had mini kitchens. I would definitely stay there again.

We also got a chance to use our semi-annual $50 Amex Resy credit at Cruz Blanca which was a combination brewery/Mexican restaurant. We had a nice meal there, but honestly I was more impressed by the drinks at Haymarket Pub and Brewery that we got before we went to Cruz Blanca. All of the beers that we tried at Haymarket were very well made and I was particularly fond of their Dopplebock. If you find yourself in the neighborhood, give Haymarket a try, it’s really good.

The kids enjoyed their illusion of freedom for a night and Alex came home with a ton of merchandise from the band. I’m glad he got a chance to see them, since they were not going to be in our town anytime soon.

This is really the kind of thing that we wouldn’t have done without points and miles since the cost of a couple of hotel rooms, dinner and driving up to Chicago would seemed too much for him to just see his favorite band. However, because we were able to redeem points and a certificate the cost was low enough to go ahead and say yes.

Alaskan Airlines Visa Signature Card

I applied for and was approved for the Alaskan Airlines Visa Signature Card. This card has an annual fee of $95 and right now has a signup bonus of 75,000 Alaska miles and a companion fare when you spend $3,000 in the first 3 months.

Outside of the signup bonus, it’s not a particularly great card for earning miles. The card earns 2x per dollar on gas, EV charging stations, transit, cable and select streaming services. It earns 1 point per dollar spent on everything else. It also has a companion fare that allows a companion to fly for $122 ($99 plus applicable taxes) round trip when you book a paid economy fare on Alaskan Airlines. An additional companion fare can be earned each year, after the cardholder spends $6,000 on the card.

That being said, I think Alaskan miles are great, and they are pretty hard to come by. They offer some really great deals on domestic flights, for example, we used Alaskan miles to book one-way American Airlines flights from Moline to Chicago for 4,500 points. That was on the same flight that we had previously booked with 7,500 American Airlines miles. Obviously we canceled the AA booking and went with Alaskan.

On to the Point Check

For the first time in a while, neither Jenn nor I wasn’t working on a signup bonus. There really hadn’t been any huge credit card offers that we just had to jump on. I did signup for the Alaska Airlines card, but I hadn’t had a chance to start using it before the end of the month.

Card Used

Spend

Points Earned

Point Value

Points Per $

Return on Spend

Citi Premier

$1,223

2,794

50.29

2.3

4.1

Amex Gold

$1150

4,327

$86.54

3.8

7.5%

Venture

$912

1,824

$33.74

2.0

4.0%

Ink Cash

$630

3,150

$64.58

5.0

10.3%

Wyndham Business Earner

$417

2,306

$25.37

5.5

6.1%

US Bank Triple Cash

$286

416

$4.16

1.5

1.5%

Total

$4,618

14,817

$260.53

3.2

5.6%

This month’s spending not devoted to earning a signup bonus

That being said, I was surprised by the fact that we had earned 5.6% as a total return with no signup bonuses. At least I know that if we stopped signing up for credit cards we’re still capable of getting more than 5% return on our spending.

With all of points earned and the two hotel rooms that were redeemed. We were left with:

203,900 American Express Membership Rewards Points

167,800 Chase Ultimate Reward Points

143,800 IHG Points

116,800 Citi Thank You Points

99,700 American Airlines Miles

71,900 Marriott Bonvoy Points

52,000 Wyndham Points

10,600 Hyatt Points

5,700 Delta Miles

2,700 United Miles

$109 in Cash Back

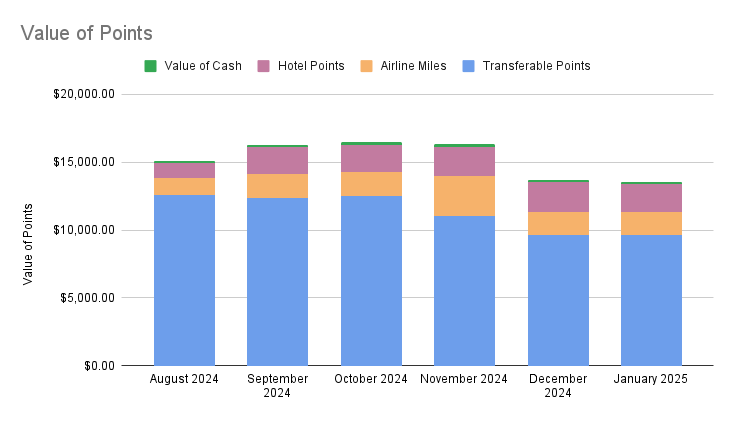

The value of all of these points and miles according to the Points Guy, totals up to $12,850 that is just a touch lower than in December. Next up will be booking for a summer trip, and I think we should have enough points and miles to make that work. After that, we won’t need to book very much because we would have three trips for 2025 already booked. Sounds ridiculous, but that’s okay with me!

I am a travel hacker, and the amount of travel I do is unusual. We traveled three times last year, including a week in Canada, a week in Costa Rica, and a week and a half in Italy. I also had a extended weekend trip to Montana with my old high school friends. I do realize that this isn’t normal and it’s also a lot more than we did even a few years ago. We also did that without spending a lot of money, because of points and miles.

Most Americans, if they travel at all, probably plan just a single vacation a year. If you only travel once a year, though, you really want to make the most of it. This is where doing a little bit of travel hacking would allow you to stretch your budget and allow you to travel with a little more panache.

The average American who wants to take one trip per year, should maximize that trip as much as is possible by using a one credit card per year strategy. This gives the average traveler the ability to reduce the cost of their vacation or increase the luxury of the vacation without having to become a crazy travel hacker.

Why New Accounts are Important

Let’s say that you already have a Chase Sapphire Preferred card. It’s a great card with good earning categories and great benefits. Why would you need anything else? Well, the truth is that signup bonuses are really important to building point balances. In the case of the Chase Sapphire Preferred card, if you spent $3,000 per month on that card, you would probably earn around 4,000-4,500 points, depending on what categories most of the spending was in. That means that at the end of the year, you would have earned somewhere around 50,000 points on $36,000 in credit card spend.

The signup bonus for the Chase Sapphire right now is 60,000 points. That means that if you signed up for the card and did the above spend, you would end up with 110,000 Ultimate Reward points. For 50,000 points, you can probably eek out enough points for 2 to fly to Cancun, if you’re flexible on when you fly. For 110,000, you can fly to Cancun and stay in an All-Inclusive hotel for 2 or 3 nights. For 110,000 points you could also pretty easily fly 2 people to Europe and back, if you transferred those points to KLM/Air France Flying Blue, or Iberia/Air Lingus/British Airways/Finnair Avios. If you were only paying for one flight, you could probably get to New Zealand and back for that, but that’s a long flight in economy.

Signup Bonus Frequency

The problem is that you can’t sign up for the Chase Sapphire Card each year. Chase only allows for you to get a signup bonus on the Sapphire Card once every four years. The same is also true of the Capital One Venture Card and the Citi Strata Premier Card. The American Express Gold Card is technically for a lifetime, but apparently people do get a second bonus on that card, usually after around 7 years.

I mention these cards because they have transferable points, meaning that you can earn them as Citi Thank You points, Chase Ultimate Reward points, Capital One Venture miles or Amex Membership Reward points and you can transfer them to any of their hotel and airline partners to take advantage of their best deals.

It’s also fortunate that there are four of these cards and with the exception of the Amex Gold card, you can get an additional bonus once every four years. This means that you can signup for one of these cards, earn as many points as you want during the year, transfer the points out and either downgrade or cancel that card and move on to the next card in this group. With the exception of the Amex Gold card on the 4th year, you could rotate though those cards every year.

Work With a Friend

While solo travel can be fun, traveling with a spouse, significant other, or a friend can make trips extra special. Working together to earn points also makes for a great strategy. In the travel hacking community, they affectionately call this ‘two player mode’.

Let’s say that you’re married and your spouse will be traveling with you. Two player mode essentially works like this: You sign up for the Citi Strata Premier card. You do the required spending and earn your signup bonus, but you DO NOT add your spouse as an authorized user. Then your spouse signs up for the same card and earns the same bonus. After both of you have earned your bonuses you continue to use those cards for all of your credit card spend for the rest of the year.

In two player mode, assuming the $3,000 per month spend listed above, in addition to the 50,000 or so points you would earn on your normal spend, you would also earn two 75,000 point sign up bonuses. That would mean a total of 200,000 Citi Thank You points that can be used to vacation in a variety of places.

Citibank’s Transfer Partners

If you just used Citi Thank You points to pay for items on your card, you would get .8 cents per point for a total of $1,600 for those 200,000 points. Don’t do that. The best way to use those points to transfer to airline partners and purchase flights. Citi has quite a few transfer partners. They are:

Partner

Citi Points Used

Points Received

Aeromexico Rewards

1,000

1,000

Accor Live Limitless

1,000

500

Avianca Livemiles

1,000

1,000

Cathay Pacific

1,000

1,000

Choice Privileges

1,000

2,000

Emirates Skywards

1,000

1,000

Etihad Guest

1,000

1,000

EVA Air

1,000

1,000

Air France/KLM Flying Blue

1,000

1,000

Jetblue Trueblue

1,000

1,000

Leaders Club

1,000

200

Preferred Hotel and Resorts

1,000

4,000

Qantas Frequent Flyer

1,000

1,000

Qatar Privilege Club

1,000

1,000

Singapore Airlines

1,000

1,000

Thai Royal Orchid Plus

1,000

1,000

Turkish Airlines Miles and Smiles

1,000

1,000

Virgin Atlantic Flying Club

1,000

1,000

Wyndham Rewards

1,000

1,000

This list can be a bit overwhelming, but if you spend a little effort you can use these transfer partners for some great value. There are too many great uses of these points to discuss all of them but I’ll give you some surprising examples:

Using Turkish Airlines Miles to Fly To Hawaii on United Airlines

This is one of those bizarre combinations that works pretty well if you are flexible about when you go to Hawaii. You do this by finding saver awards to Hawaii on the United Airlines website. Once you find this then you search on the Turkish Airlines Miles and Smiles website for Star Alliance award space for the same day. Usually if saver awards are available on the United website, you will find it on Turkish Airlines for 10,000 points each way. If you used United miles, it’s probably going to be 25,000 miles.

Flying Blue used to offer a lot of flights to Europe for an extremely low 20,000 points. A recent devaluation happened that has raised that price to 25,000 points. There are some great things about this program. One is that it covers both Air France, which uses Paris as its hub, and KLM, which uses Amsterdam as it’s hub, making a single platform that covers both airlines’ reward programs. The second thing is that it covers a whole lot of award flights to Europe from the United States. Using the Daydream Explorer feature in PointsYeah, I came up with a ton of 25,000 point flights to Europe in May.

However, one of my favorite things about Flying Blue is that it allows for stopovers in Paris and Amsterdam. In other words, if I’m flying from Chicago to Munich on KLM, there is going to be a stop at it’s hub in Amsterdam. I can choose to do a stopover for up to a year in Amsterdam before moving on to Munich. This allows me to book one flight to Munich, pay one fare, and stay in Amsterdam for a few days, a week, whatever I feel like doing. The bad news is that there isn’t a way to do it on the website, you’ll have to call. The worse news is that if you book with an agent on the phone, it costs 50 Euros per ticket. That being said, I’ll gladly pay 50 Euros for a stopover in Amsterdam.

East Coast to London on Virgin Atlantic

I honestly can’t believe this hasn’t dried up yet, but for some reason Virgin Atlantic offers flights from mostly JFK airport in New York to London for 6,000 points and around $70 in taxes. They also have the same prices for some flights from Washington Dulles and Boston Logan, but most are from New York to London. It seems to be too good to be true, so get it while you can, I guess.

Qatar Privilege Club for Transferring to Avios

I really like the Avios program. It is a points platform that is used by Qatar Airlines, British Airways, Iberia Airlines, Aer Lingus and Finnair. In the case of Citi, it only transfers to Qatar, but once you transfer points to Qatar you can transfer to these other programs, although it can get a little complicated, One Mile at a Time has a good explanation of how to do it.

Once you convert your Citi Thank You points to Avios, you can use them for such things as 13,000 point off peak flights from most of the eastern portion of the US to Dublin, 17,000 points from Chicago to Madrid off peak on Iberia Airlines, and 30,000 points to Helsinki from the US. These are obviously not always the prices, but they are fairly typical, and available if you are flexible.

Other Examples

There are some other transfer partners that can be very useful as well. If I were booking anything to Central America, South America, Mexico, or the Caribbean, I would start my search with Avianca Lifemiles. They consistently have competitive prices to those areas. I recently saw an example of 14,000 points and around $65 to San Jose del Cabo from Chicago.

Keep your eyes on JetBlue as well. There is a new partnership with TAP Portugal where you can get to Portugal from the United States for as low as 19,000 miles and $5.60 using JetBlue Trueblue miles. The Points Guy went into depth on this new sweet spot, and I think I’m going to have to look into that one a little more, it sounds very promising.

Citi’s Hotel Partners

While I love the choices for transferring to Airline partners, Citi’s hotel partners aren’t as exciting. You can get some value by transferring to Choice hotels at 2 Choice points per 1 Citi Thank You point. You could also transfer to Wyndham and take advantage of their partnership with Vacasa that has been a little watered down, but it’s still pretty good.

For the most part, though, the best use of Citi points will be to book flights, so I would hesitate to transfer to hotel partners in less you found a great use for those points. Of course you should never feel bad if you choose to use your points in a suboptimal way, since they’re your points and you should use them the way you want, but making the most out of your points will help stretch your vacation budget.

How Much Can This Save You?

If you are only going to take advantage of one signup bonus per year, it becomes imperative that you do everything you can to maximize the use of those points. This is where you should spend your mental energy. The good news is that there are a ton of resources on how to take advantage of these transfer partners to get the most of those points.

I suggest using PointsYeah as a good place to start. You can search a number of airline programs simultaneously so that you can choose where to transfer your points an book your flights. Also, sometimes just spending a few minutes googling for the best use of points for flights to the destination you want to go to will yield you a blog article that will be very beneficial.

So how much can you actually save doing this? Let’s look at the example of a couple in two player mode that earned 200,000 Citi Thank You points. From the examples above, probably the easiest, and most available redemption opportunities would be to book two sets of one way flights to Europe using Flying Blue. If they had a family of 4, they could book one set of flights on KLM with a stopover in Amsterdam and then head on to Munich. On the way back, they could book a flight with Air France and stop for a few nights in Paris. In this example, the family of four would spend 50,000 points and around $300 in taxes and surcharges each. Those flights probably would normally cost over a $1000 each. I would imagine that this would save the couple around $3,000 on this trip.

In the Turkish Miles and Smiles example above, booking from the US mainland to Hawaii for 10,000 points each way would mean that for 200,000 points that couple could book 10 round trip tickets. Those tickets typically cost between $600 and $1,000. So in this example it could save the couple between $6,000 and $10,000.

The amount that you save is definitely going to vary by location and airline, but it can definitely stretch that vacation budget out to save money on the flights.

A Simpler Way to Travel Hack

By using a one card per year strategy, you can reduce the cost of your vacations without putting too much of an effort into it. Juggling multiple credit cards to maximize point accumulation in bonus categories and having multiple signup bonuses per year takes work and mental energy. Most people would prefer to not have to think so hard about which credit card to swipe on every single purchase.

By signing up for one card per year, you can take advantage of the signup bonus and continue to use that card throughout the year. The key is to be smart when redeeming those points with transfer partners and Citi Thank You points have some really great transfer partners. Doing this one thing, can save you thousands of dollars per year on your travel plans. It can also be the key to unlocking vacations that you wouldn’t have considered before. Doing just a little travel hacking absolutely has the potential to open the entire world to you.

December is always a month to get together with family and friends to celebrate the holidays. For a lot of people there is holiday travel, but this has always been a time for us to stay home. Now that we’ve been traveling more, this is time that I get a chance to slow down and think about next year’s travels.

While children dreamed of Christmas morning, I was dreaming about where we are going in 2025. Over the last few years, we have done a great job of building up our point balances in a variety of programs, and that opens up a lot of possibilities for our 2025 travels.

It has been tempting to think of places in South America or Asia, but right now, we really love going to Europe. Even though it can be a challenging distance to fly, it’s still close enough that a seven to ten day trip isn’t dominated by flights and the accompanying jet lag. The infrastructure of subways, high speed rail and airports makes getting around in Europe without renting a car easy.

Europe is beginning to feel like an easy destination, where I don’t have to worry too much about how to get around, where to stay or for that matter the language barrier, since so many Europeans speak English well. Plus, we have so much left to see in Europe. Because of that, we have three trips to Europe in 2025 in various stages of planning.

Redemptions Galore

I went on a bit of a booking spree in December. It started with me noticing a great deal on an American Airlines flight to Nice at the perfect time for the UTMB Nice Cote d’Azur Ultramarathons. I wanted to do the 54 kilometer trail race, but I also wanted to make sure that I could get a decent price on a flight before I committed to it. We booked the way there from Moline for only 19,000 American Airlines miles and $11 each. Getting home wasn’t quite as affordable as going to Nice, so I ended up booking a flight out of Dublin, Ireland instead for 19,000 American Airlines miles and $47 in taxes.

That meant we needed to book a flight from Nice to Dublin which we were able to secure on Aer Lingus for a 6,500 Aer Lingus Avios and $37 each. We transferred Amex Membership Rewards points to Aer Lingus Avios at a 1:1 ratio to acquire the necessary Avios. So in the end, for Jenn and I to fly to Nice from Moline and then on to Dublin for a couple days and then back to Moline, cost us 76,000 American Airlines miles, 13,000 Amex Membership Reward points and $190 in cash.

In November, we had booked a flight for Jenn and I and our two kids Alex and Emma from Chicago to Porto, Portugal for 48,000 Virgin Atlantic miles transferred from 35,000 Chase Ultimate Reward points and $702 in taxes and fees.

We did however, need to get back so we booked 4 flights from Madrid to Chicago for 88,000 Iberia Avios and $512 dollars in taxes and fees. Those points were transferred from American Express Membership Reward points and we used 50,700 Capital One Venture miles at one cent per point to wipe out all but $5 of the taxes and fees.

So in two months we booked four flights from Chicago to Porto, four flights from Madrid to Chicago, two flights from Moline to Nice, two flights from Nice to Dublin and two flights from Dublin to Moline. These flights in total cost us 101,000 Amex Membership Reward points, 76,000 American Airlines miles, 50,700 Capital One Venture miles, 35,000 Chase Ultimate Reward points and $897 in cash. I was able to redeem $875 in cash back to help out with the cash for taxes and fees, so out of pocket these flights cost us a grand total of $23. I’m not mad about that at all.

The cash value for the flights from Chicago to Porto were $433 each on KLM. The cash value for the flights from Madrid to Chicago on Iberia was a shockingly high $901 each. The whole Moline to Nice to Dublin to Moline itinerary had a cash value of $1,253 each. The grand total for all of that would have been $7,842 so to only fork over $23 isn’t bad. The 262,700 points and miles we used ended up netting us over 2.6 cents per point in value which is way above what they are actually valued at, so we did a tremendous job of redeeming those points.

A Couple of Bonuses

The $875 in cash back didn’t appear out of thin air. I happened to finally get my $750 sign up bonus for hitting the required $6,000 in spend in the first five months of opening my US Bank Triple Cash card. I actually spent a little over $6,400 and the total cash back was over $850. That meant I got around 13.3% cash back for all of that spend on the Triple Cash over the first 4 months. That’s pretty good, I’ll take it.

Jenn also hit the signup bonus that she was working on. She signed up for the Citi Strata Premier card, which had a 75,000 Thank You point bonus after spending $4,000 in the first 3 months.

This leaves us with no current credit card signup bonuses we are working on, so I’ll have to make a decision about how I’m going to go about building up our points balances after using so many in the last couple of months.

Never Forget Those Credits

I’m supposed to be an “expert”, right? Well, I was listening to a podcast (It was probably Frequent Miler on the Air), and they mentioned that you need to make sure to use up the credits that were expiring at the end of the year. One of the credits that they mentioned was that many Delta Airlines credit cards have hotel credits that can be used once a year. I knew Jenn had a Delta Airlines Business Gold card and so I checked out the credit. Sure enough, there is a $150 annual hotel credit if you book the hotel though Delta Stays.

We used the credit to do a short trip to Iowa City for an Iowa Hawkeye Women’s Basketball game – Go Hawks! We also use this as an opportunity to use up the $50 semi-annual Resy credit that comes with my American Express Gold card.

This was a huge reminder to me to make sure that I not only understand all of the benefits of the credit cards we have, but to actually use them. Most travel credit cards with annual fees will have some benefits or credits that will expire if you don’t use them. It’s important to remember to use those, or you’re not getting the full benefit of a card you’re paying for.

On to THe POint Check!

We didn’t stray too much from the cards that we were working on for a bonus this month. Most of the spending that we did on cards not earning a signup bonus was on recurring charges like utilities, insurance, streaming services, etc. The good news is that you can get a pretty good return on that spend and we were able to get a fairly impressive 7.1% return on all of those recurring charges last month. I’ll take it.

Card Used

Spend

Points Earned

Point Value

Points Per $

Return on Spend

Ink Cash

$463

2,317

$47.50

5.0

10.3%

Wyndham Business Earner

$450

2,591

$28.50

5.8

6.3%

Venture

$345

690

$12.77

2.0

3.7%

Total

$1,258

5,598

$88.76

4.4

7.1%

This month’s spending not devoted to earning a signup bonus

Besides the spending listed above, I also spent a little over $2,200 on my US Bank Triple Cash card earning $37 in cash back as well as the $750 sign up bonus. Jenn spent a little over $2,800 on her Citi Strata Premier card and earned almost 5,600 Citi Thank You points as well as the 75,000 point bonus on that card.

After earning two bonuses and having a whole lot of points redeemed for flights, we were left with:

199,600 American Express Membership Rewards Points

176,700 Chase Ultimate Reward Points

142,300 IHG Points

113,900 Citi Thank You Points

99,700 American Airlines Miles

71,900 Marriott Bonvoy Points

49,700 Wyndham Points

19,600 Hyatt Points

5,100 Delta Miles

2,700 United Miles

$105 in Cash Back

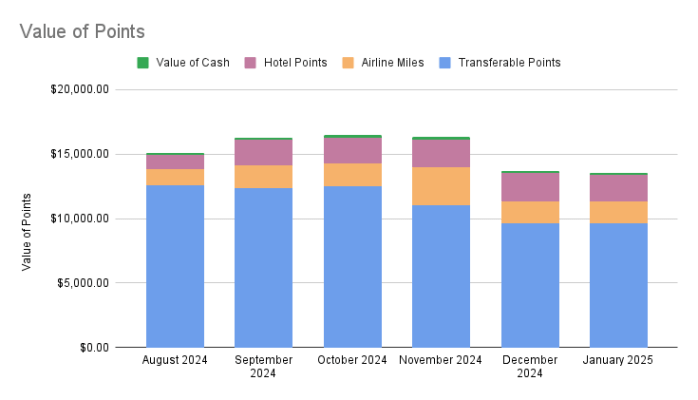

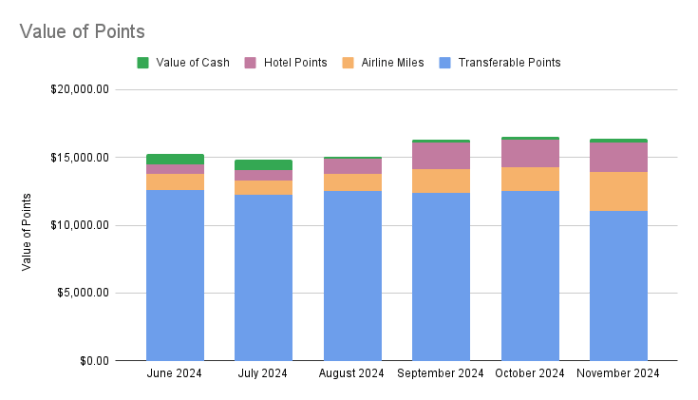

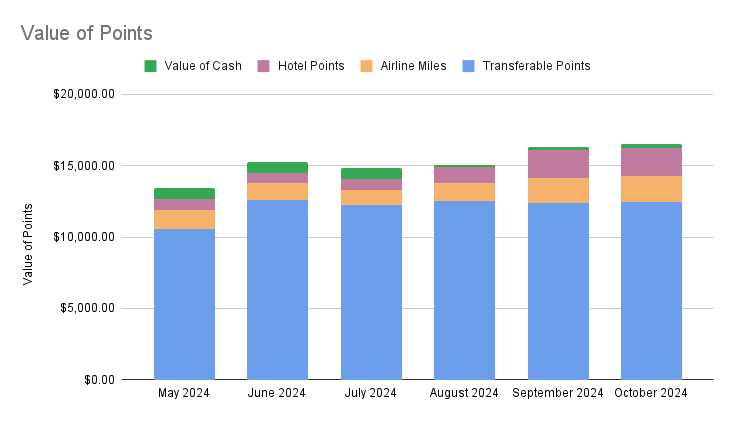

According to the valuations published by The Points Guy, the total value of our points, miles and cash back is $12,950. That is a significant drop from November when the total was worth $15,600, but that’s fine. We are using those points wisely and have all of the flights for two trips to Europe out of the way. I just need to book a summer trip and all of our plans are ready for 2025. It’s going to be a fun year.

November was a pretty good month for us. Why? Well we were in Italy for a couple weeks of it. Italy is a magical place where climate, landscape, food, culture and history all come together to make an incredible place to visit. There is no doubt why it is one of the most visited countries in the world and it did not disappoint.

We stayed in Florence, Venice and Rome and we also had a nice day trip to Cinque Terre. Rome and Venice were repeats for us. Rome is fine, I’m sure we will visit again, but I’m amazed by how much we’ve enjoyed Venice. Before we went the first time, I thought Venice would feel extremely touristy. It turned out to be quite different than I imagined. It really felt more authentic than the other places we visited. That being said, I think we spent more time on the side streets away from the tourist traps than the other cities we visited. It’s a reminder to us to actively get away from the main tourist areas of a city.

I’m determined to revisit Cinque Terre, hopefully for a few days. I’d love to hike the trail between the five towns and really spend some time exploring each of them. A day trip just wasn’t enough to fully appreciate Cinque Terre. As far as Florence is concerned, it’s the most beautiful city I’ve visited thus far, but even during the off-peak travel season, it seemed overrun with tourists. I might have appreciated Florence more if we would have wandered out of the main tourist areas.

A Couple of Redemptions

We have three trips planned for next year. The first is a spring break trip to spend a week on the Portuguese route of the Camino de Santiago de Compostella. The second trip is a summer trip where we haven’t determined locations or dates. The third is a trip to Nice France to participate in a UTMB trail running event where Jenn and our friends Bill and Theresa will be doing the 22 kilometer race and I will be participating in the 54 kilometer race.

In November, we started the planning of these trips by booking a flight from Chicago to Porto. Virgin Atlantic was charging 12,000 miles and $175 per ticket to book the flight but with a 40% transfer bonus from Chase it ended up costing us 35,000 Chase Ultimate Reward points and around $700 for four tickets.

In cash, those flights would have cost $433 each. That means that we ended up getting a little over $1000 value for those 35,000 Ultimate Rewards points. That works out to 2.9 cents per point value, when Chase Ultimate Rewards points are typically valued at 2 cents per point so I’m pretty happy with the redemption.

We also used 38,000 Capital One miles to wipe out the cost of some train tickets from our trip to Italy. This isn’t the best use of Capital One miles, because we just get one cent per point on reimbursement for travel purchases. However, my goal is to use all of Jenn’s Capital One miles so she can cancel her Venture Card and then I will apply for one. Capital One allows people to get a bonus every four years so I think with the two of us working together, the smart thing is for us to alternate every two years who is carrying a Venture Card. That will allow us to maximize signup bonuses for Venture cards.

Barclays Aviator Red Bonus

I had one signup bonus hit in November. I received the 70,000 American Airlines mile bonus for signing up with the Barclays Aviator Red card, which is scheduled to no longer be with Barclays in 2026. This is part of an exclusive deal between American Airlines and Citibank, making Citibank the exclusive bank of all of the American Airlines credit cards moving forward. Customers who hold American Airlines cards issued by Barclays will probably be transferred to Citibank and I would assume that the Aviator Red card will no longer be taking new applicants. Therefore if you if you want sign up for the Aviator Red card, the clock is ticking, and I would assume that some time soon, Barclays will no longer be taking new applications.

On to the Point Check

I’ve been working on a signup bonus for my US Bank Triple Cash card and I had some issues with it that really boils down to me not paying attention to what I was doing. Without getting into the boring details of it, I’m an idiot and I ended up having to get new credit cards issued, with the correct business name on it. This happened right before we went to Europe, so I basically wasn’t using the card for most of the November billing period.

Card Used

Spend

Points Earned

Point Value

Points Per $

Return on Spend

Amex Business Gold

$889

1401

$28.02

1.6

3.1%

Amex Gold

$817

2,148

$42.96

2.6

5.3%

Venture

$752

1,504

$27.82

2.0

3.7%

Citibusiness AAdvantage

$698

698

$11.17

1.0

1.6%

Ink Cash

$459

2,298

$47.11

5.0

10.3%

Wyndham Business Earner

$422

2,288

$25.17

5.4

6.0%

Total

$4,046

10,337

$182.25

2.6

4.5%

This month’s spending not devoted to earning a signup bonus

My spending primarily got put on my Amex Gold and the Citibusiness AAdvantange, where they didn’t take American Express, which was in a lot of places in Italy. It wasn’t really ideal, and that’s why my non-bonus spend only returned a disappointing 4.5% last month. I ended up spending less than $500 on my Triple Cash card and earned about $8 in cash back.

Jenn has been working on her bonus for her Citi Strata Premier card and spent less than $1,500, earning over 2,500 Citi Thank You points.

Between the points earned this month and the redemptions the total value of our points went down slightly. We finished the month with:

298,200 American Express Membership Rewards Points

175,700 American Airlines Miles

174,300 Chase Ultimate Reward Points

142,300 IHG Points

71,900 Marriott Bonvoy Points

48,900 Capital One Venture Miles

47,100 Wyndham Points

19,600 Hyatt Points

5,000 Delta Skymiles

2,700 United Miles

$227 in Cash Back

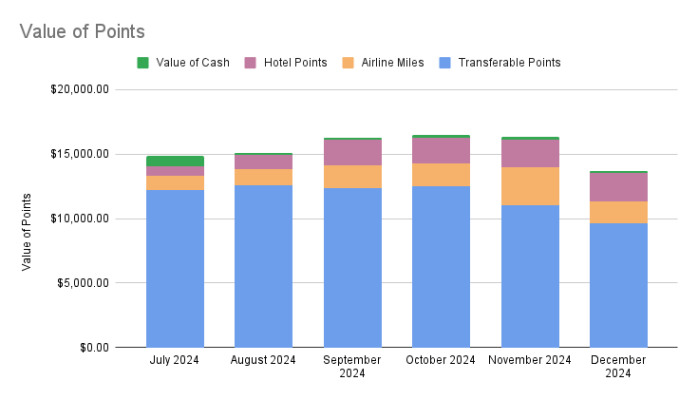

All of these miles, when using the Points Guy’s valuations, add up to around $15,600. That should give me plenty of room to do all of the travel planning that I need to do for 2025. That’s the fun stuff, I can’t wait!

I love my local airport. It’s MLI, sometimes known as the Moline Airport or as it’s officially called, the Quad Cities International Airport. What is great about this airport is that you can pretty much roll into a parking spot 20 minutes before boarding and be alright. I personally am not brave enough to try it, but I’m certain you’d be fine. TSA normally takes less than ten minutes and you can literally park just a couple hundred feet from the front door. There are only a dozen gates, so it only takes a couple minutes to get to your gate. Whenever it’s feasible, we try to fly out of MLI. If we can’t, we generally fly out of Chicago O’hare.

On the other hand, I really hate the whole experience of going to Chicago O’hare. It’s a three hour drive and the last hour is in white knuckle traffic. Then we have to park something like a dozen miles away and take a shuttle to the airport. Getting to O’hare is usually a four hour ordeal for us and we have to leave at least two hours for security and getting to the gate. There is nothing pleasant about having to leave your house six hours before boarding.

Booking award flights out of MLI however, is a little tricky. Flying to Europe on points, we usually find the best deals on KLM/Air France Flying Blue or with either Aer Lingus or Iberia Avios. None of those airlines fly out of MLI, but they all have direct flights from Chicago O’hare to Europe. There are only three airlines that will book with points out of MLI: United, American, and Delta.

This leaves us with three choices. The first is to book with one of the European carriers and deal with the whole ordeal of driving to Chicago. This isn’t great, not only because of the way there, but generally that means we’re trying to stay awake while driving home after a seven hour time change when returning from Europe.

The second option is to book a separate award flight to get to Chicago and book with a European carrier out of Chicago. The problem with the second option is that if something happens to your first flight, such as a delay, the second flight doesn’t care that your first flight is delayed, since it’s not their fault and frankly not their problem. When I’ve done this in the past, I’ve booked a day early just so we could make sure to get there in time.

The third option is to book the whole trip with one of the American carriers that fly out of MLI. The problem with the third option is that it’s often a whole lot of points. United Airlines consistently charges a premium for flying to a small airport, and I usually just look at their prices and laugh. Delta rarely has good award prices and when you find a deal you need to book them as a round-trip ticket to get good rates. American Airlines, however, continues to surprise me with great value on award flights out of MLI, although you do have to hunt a little for them.

Punishing Myself in Style

I’ve been a distance runner for about eight years now and I’m turning 50 next year. I decided that as a challenge to myself, I would run my first 50K during my 50th year. But let’s face it, I’m a travel hacker, if I’m going to do a 50K, of course I’m going to do it with a little style.

I decided to do the 50K which is one of the UTMB ultramarathons that are taking place in Nice, France. The race in the 50K category in Nice is actually a 54K with around 7,000 feet of elevation gain. This is going to hurt – honestly it’s probably bordering on self-torture. But hey, If I’m going to torture myself, why not do it in the hills overlooking Nice, Monaco and the Mediterranean Sea, right?

Searching for Flights

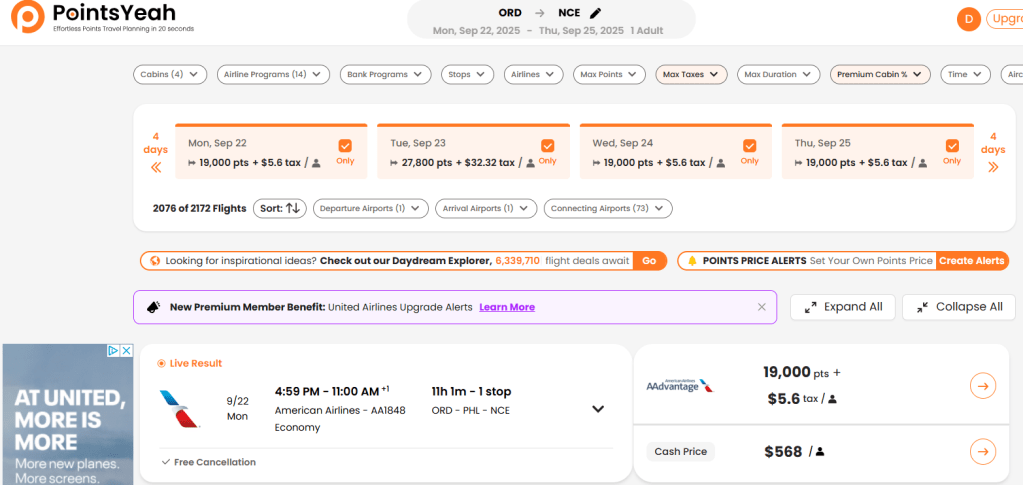

Now that I knew what I wanted to do, I needed to get there. I started my search the same way that I always do, by searching on PointsYeah from Chicago to wherever I want to go, in this case the Nice Airport, NCE. Right away I noticed that American Airlines had a 19,000 mile award from Chicago to NCE.

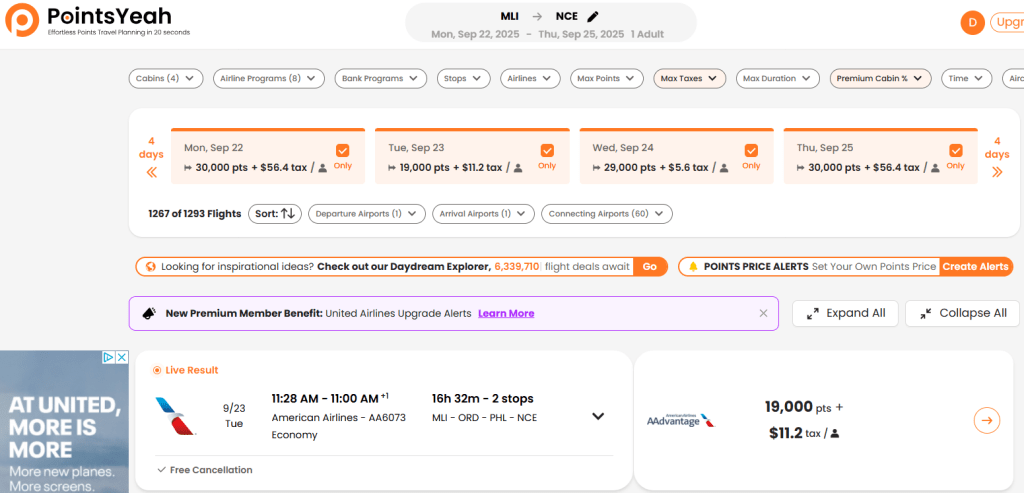

If I see that any of the major American carriers have a cheap flight from Chicago, I instantly change it to MLI, just to see if they also have a cheap flight to the Quad City Airport. Sure enough, American tacked on an extra leg and it was still 19,000 points and $11 in taxes. I immediately jumped on that.

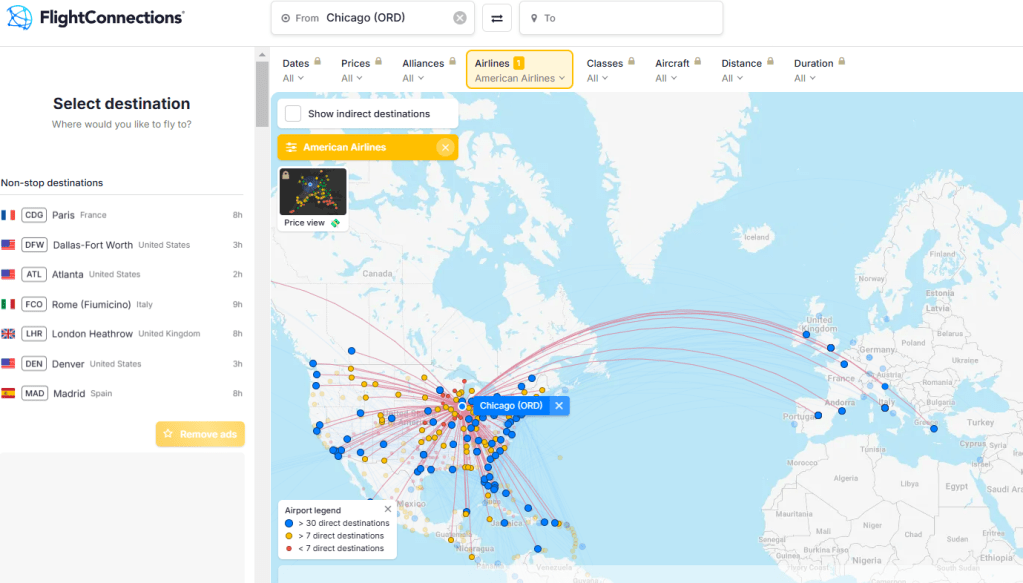

Flying home, the best I could find was again an American Airlines flight from NCE to MLI for 30,000 points and $130 in taxes and fuel surcharges. Honestly, that’s not bad, but I decided to look around a little bit. I went on Flight Connections and filtered down to see where American Airlines flew directly from Europe to Chicago, knowing that there are multiple flights from Chicago to MLI every day.

I then used PointsYeah to check each of these cities to MLI to see if American Airlines had any other great deals. I wound up finding a flight from Dublin to MLI for 19,000 American Airlines miles and $47. This of course means that we will have to get from Nice to Dublin, but Aer Lingus is available for 6,500 Aer Lingus Avios and $37 in taxes.

Why would we position ourselves to a different country just to fly home? Well, I always like a bargain, but this also means we can spend a day or two in Dublin. I love the idea of having a stopover like this, because it really gives you a quick sample of a city so that you can know whether or not you would like to return later. Honestly, I feel like being cheap can actually make your trips better.

What We Are Paying Vs Cash Flights

Once we book the flight with Aer Lingus, which I’ll book for 6,500 Amex Membership Rewards points transferred to Aer Lingus Avios and $37 in taxes, we will have essentially booked the entire trip for 38,000 AAdvantage miles, 6,500 Membership Rewards points and $95 in fees for each ticket.

Booking the American Airlines portion of the flights with cash would have cost $1,091 if we booked it as a multi-city flight with an open jaw (a flight itinerary where you fly back from a different city from where you landed). The cost of the Aer Lingus flight was $162 for a one way flight from Nice to Dublin. Together, the itinerary was $1,253 booking with cash. That means we got a value of 2.6 cents per point for our award flights. Considering The Points Guy values American Airlines miles at 1.65 cents per point and Amex Membership Rewards points at 2 cents per point, I’d say we did pretty well on that redemption.

Creativity and Thrift Wins Again

When we first started travel hacking, we didn’t have a lot of points to throw around for our trips. On our first trip to Europe, we had to fly back from Stockholm because that was the only flight we had enough points to book, even though we were going to be in Italy. We ended up having to book a separate flight from Rome to Stockholm to make it work. It turned out to be great though, because we got to experience Sweden for a few days. It taught me that thinking outside of the box can allow you to enhance your trips while essentially being cheap.

This time we had the points to fly back directly from Nice, but by being creative with how we booked our flights, it allowed us to retain more of our valuable American Airlines miles and we were able to tack on a side quest to Ireland. Enhancing our trip while getting great value is a win win, even though after running the 50K, I probably won’t be able to walk by the time we get to Dublin.

Much of our time in October was spent preparing for our trip to Italy. Our trip included our good friends Bill and Theresa and Jenn’s Parents. None of them had been to Italy before and we wanted to make sure that they had a great time. I spent a decent amount of time researching places to visit, things to eat, train tickets, etc.

Meanwhile, Jenn spent a good deal of the month making ensuring that our kids had everything they needed to survive while we were gone. Emma and Alex are 19 and 15, respectively and they are definitely at the age where leaving them for another continent is questionable. I am, however, a firm believer that giving children challenges is a great way to turn them into functioning adults.

I can tell you that Emma passed this challenge with flying colors. She was not only responsible for taking care of Alex while she was gone, but she also was working, going to school and taking care of Jenn’s Parents’ dog. On top of that, she was coaching a youth basketball team. She took care of all of that and made sure that our house didn’t turn into a scene from Lord of the Flies. We couldn’t be prouder of her.

Citi Strata Premier Card

Right before we left for Italy, Jenn applied for, and her application was accepted for the Citi Strata Premier card. This is Citibank’s premier card and it’s a pretty good one. It has a $95 annual fee and has some pretty good bonus categories.

10x on Hotels, Rental Cars, and Attractions booked through the CitiTravel.com

3x on Groceries

3x on Restaurants

3x on Gas and EV Charging stations

3x on Flights and Other Hotel Purchases

1x on Everything Else

Getting 3x on groceries, restaurants and gas means means the cardholder can get 3x on a large portion of their spending without worrying about using one card for dining, and one card for gas, etc. It is a great credit card for people who don’t want to think too hard about points and miles.

This card currently has a 75,000 point welcome offer when the cardholder spends $4,000 within 3 months. Citi points are valued at 1.8 cents per point by The Points Guy, so that bonus is worth $1,350. In order to get that 1.8 cents per point value, you would need to use one of Citi’s transfer partners, including some of my favorites like Air France/KLM flying blue and Avianca Lifemiles.

It has a $100 credit on a hotel purchase of $500 or more using the Citi Travel site. It also has some trip protections and no foreign transaction fees. Overall, it’s a really solid travel credit card and especially good for people who don’t want to manage multiple cards.

Ok, On to the Point Check

This was not a great month for spending on non-bonus cards. We’ve gotten a little lazy about what card to use. For the vast majority of the month, Jenn didn’t have a card where she was working on a signup bonus. She is usually the one yelling at me that we need to sign up for a new card, because she can’t stand not working towards a signup bonus. Because she didn’t have a signup bonus to work towards, she just used her IHG Premier and her Amex Business Gold, neither of which were particularly great choices.

Card Used

Spend

Points Earned

Point Value

Points Per $

Return on Spend

Amex Business Gold

$1,143

1,310

$26.20

1.1

2.3%

IHG Premier

$814

2,695

$13.48

3.3

1.7%

Ink Cash

$561

2,783

$57..05

5.0

10.2%

Venture

$372

745

$13.78

2.0

3.7%

Wyndham Business

$284

1,588

$17.47

5.6

6.2%

Total

$3,174

9,121

$127.98

2.9

4.0%

This month’s spending not devoted to earning a signup bonus

Because of that, the return on spend on cards where there wasn’t a signup bonus was 4%. I like to keep that number above 5% and lately we’ve been over 6%. Note to self – make sure Jenn has a signup bonus to work on.

Besides the spending on the above chart, I spent over $3,200 on my US Bank Triple Cash card, earning a little under $50 in cash back. That puts me more than halfway to the $6,000 in required spend to earn the $750 bonus on that card.

That meant that we finished the month with:

296,700 Amex Membership Reward Points

217,000 Chase Ultimate Reward Points

141,700 IHG Points

104,800 American Airlines Miles

85,400 Capital One Venture Miles

71,900 Marriott Bonvoy Points

30,400 Citi Thank You Points

11,300 Hyatt Points

5,000 Delta Miles

2,700 United Miles

$220 Cash Back

Using the Points Guy’s valuations, all of this totals to an all-time high for us of $15,800 in points, miles and cash back. We have some pretty big travel plans for 2025, so we’re going to need a big stash of points available. Hopefully I see some Black Friday deals so I can lock in some plane tickets!

Amsterdam is a city that I’ve dreamed of visiting for decades. The center of Amsterdam is a magical area where the canals and the buildings that line them are practically frozen in the 17th Century, when merchants trading goods from Asia brought wealth to the Netherlands. It was amazing to visit Amsterdam, even though it was a short stopover.

Taking Advantage of KLM Stopover Rules

We had the opportunity to take a 25 hour stopover on our way to Rome. When we planned our trip to Rome, there was a flight we liked from Chicago to Rome, but the layover in Amsterdam was only a little over an hour. That was a dangerous connection since we would have to go through immigration and security. We might’ve made it, but any delay would have made it close to impossible.

Our solution to the short layover was to fly in a day earlier and use KLM’s stopover rules to our advantage. KLM gives flyers the ability to stop in Amsterdam for up to 12 months on flight itineraries that stop in Amsterdam. This adjustment meant that we had a day in Amsterdam to defeat jet lag and do some wandering.

The KLM flight from Chicago to Amsterdam was comfortable and we landed at the airport without incident. Amsterdam has fantastic train service at the airport and in less than 20 minutes we were at Amsterdam Centraal for about 5 Euros a ticket.

Row houses along a canal in Amsterdam

We stayed at the Kimpton De Witt near Amsterdam Centraal train station. They were gracious enough to find us a vacant room and allow us to check in at around 8:30 AM. The staff was very nice and even gave us a 15 Euro drink credit for using the current Kimpton Password.

What is the Kimpton Secret Password?

Kimpton has a secret password program that allows guests to get a little something extra if they know the secret password and tell it to the clerk when checking in. It's meant to be a fun little way to create a little buzz for the hotel.

We dropped our luggage off at the room, took a quick shower and we were off and running.

Walking the Canals

We were planning to take a nap, since we, as usual, were unable to sleep on the overnight flight. But first we wanted to walk along the canals and, more importantly, get some breakfast.

Wheels of Gouda are on display at a traditional cheese maker near our hotel.

The place we stopped at was a small but very busy breakfast restaurant called Omelegg. Seating there was a bit of a challenge. We ended up having to sit next to each other at a booth because the other side had a bench that was being used by a different table. It was a little awkward, but it was fine.

The Italian Job at Omelegg

Jenn ordered the Italian Job and I got the Chicken Harissa omelette. Both were very good and served with soft slice of dark wheat bread and an arugula salad.

Row houses right on a canal. Watch out that first step out the front door is a little tricky.

The Kimpton De Witt is right on the edge of the Red Light District, so most of what we noticed at the beginning of our walk was a whole lot of weed shops and erotic boutiques. We also noticed more litter than I was used to seeing in Europe. There was a pretty pungent smell of marijuana in the air as well as cigarette smoke.

Classic Dutch Row Houses

While those things are a little unpleasant, Amsterdam is so unbelievably gorgeous it easily makes up for those shortcomings. The canal houses with their narrow five story design, brick exterior and big windows are beautiful. The tree lined canals and herringbone pattern brick streets make for an amazing backdrop for a sunny crisp fall walk.

The Church of St Nicholas

It’s nice to walk without a purpose or direction. We wandered the brick streets admiring the houseboats and tiny cars that lined the edges of the canals. It was a fairly peaceful walk with only the occasional car, bike or pedestrian that went past us. After about an hour the jet lag caught up with us and we returned to the hotel for a nap.

After our nap, we headed over to Brouwerij’t Ij. It was about a 25 minute walk from the hotel but a lot of it went through some gorgeous newer neighborhoods. Even though these neighborhoods didn’t have 400 year old row houses, the buildings kept the spirit of Amsterdam architecture. Many of them were block long buildings, instead of the narrow and tall buildings but they still were mostly 5 stories with shops on the first floor.

When we arrived at Brouwerij’t IJ I ordered a Tripel and Jenn ordered the Columbus. I loved the Tripel because it had less funk then many of the tripels that I’ve had in the past. Jenn had the Columbus which is an hoppy imperial beer which she also enjoyed. We sat out in their beer garden and watched traffic along the street which was mostly pedestrians and cyclists. It was lovely and we would’ve stayed longer but I wanted to check out Gollum Aan Het Water.

The beer and the atmosphere at Brouwerij’t Ij was great. I would recommend visiting when you are in Amsterdam.

Gollum has a series of bars around Amsterdam with an impressive beer selection, especially in bottles. Gollum was on my list of places that I really wanted to visit in Amsterdam. I was hoping to try some Belgian Ales that don’t make it to the US.

Just a portion of the amazing beer selection at Gollum Aan Het Water

We started with a Rochfort and an Orval then moved onto some regional craft beers and other Belgian Ales. The quality and variety of the beers served at Gollum was off the charts so I was a bit of a kid in a candy store.

Orval is a beer produced at Orval Abbey in Wallonia Belgium and the sale of the beer helps support the monastery.

To be fair, we had perhaps too many beers at Gollum. As is sometimes the case with us, we got to chatting with other folks at the bar. We met a nice gentleman, originally from England, and his Bernese Mountain dog as well as a couple of guys from North Carolina. The bartender was extremely friendly as well.

It’s always tough to drag ourselves away when conversation flows as easy as the beer. It’s even harder when those conversations are with interesting people from various countries.

Boats illuminated in the night.

Eventually, a little tipsy, we pulled ourselves away from Gollum we walked back towards the hotel. By this time, it was evening and the lights of Amsterdam were dancing on the ripples of the canals. Amsterdam is lovely during the day, but it’s even more enchanting at night. The wind was calm and the air was a touch chilly. It was a perfect night for a lovely walk through Amsterdam.

Montelbaanstoren, a tower dating to the 16th century is illuminated in the evening.

On our way back, we popped into a fast food Kebab place to fill up on hummus, falafel and fries. It hit the spot. I have yet to be disappointed by a middle eastern food in Europe. It is always so good and this was no exception.

Every McDonald’s in America should be replaced by Turkish Street Food – Immediately!

We Will Definitely Return

Doing a stopover in Amsterdam turned out to be a fantastic addition to our trip to Italy. It allowed us to enjoy one of Europe’s great cities without devoting a week to it.

Amsterdam did not disappoint us. Despite our initial negative reactions to the litter and smoke clouds in the Red Light District, Amsterdam is an almost magical city. The architecture, canals, the sheer volume of bikes just make for a uniquely Dutch experience.

We most definitely will be visiting Europe in the future and knowing just how great a stopover in Amsterdam can be, I think there is a good chance we will do this again. Next time, though, we might have to spend two days instead of one.

September was a fairly normal month for us. No traveling this month other than Jenn and I did spend a night in fabulous Cedar Rapids, Iowa at the luxurious Residence Inn. I know that sounds funny, but we had an expiring Marriott hotel certificate. Unfortunately, we just didn’t find a use for it until it was close to expiring.

The funny thing was we just didn’t want to drive too far for a one night stay, and the only places that seemed interesting enough to drive to within a couple of hours was Cedar Rapids and Iowa City. It was the day of the annual Iowa Hawkeyes/Iowa State Cyclone football game so finding a good use for that hotel certificate anywhere near Iowa City on that weekend was tricky, since the hotels were pretty full.

We ended up staying in a hotel that frankly was a little run down, but it was fine and we had a little night out in Cedar Rapids. It was fun to visit a city nearby that we hadn’t had a chance to experience yet. It was also a good reminder to stay on top of those free night certificates.

The flights now cost a grand total of 18,000 Amex Membership Reward points and $72 instead of the original 30,000 American Airlines miles and $22. Since I really value American Airlines miles, I was glad to have those returned.

Keeping It Loosey-Goosey

I’ve been spending a decent amount of my time getting ready for our trip to Italy. When we went to Europe last summer, I made sure to book all of our train tickets, museums and tours in advance. That was necessary, in my opinion, during high season. This time we’re going during November, which I’m hoping means that we can be a little bit more relaxed about our schedule. It is a bit of a gamble, but I think it will pay off.

The way I see it, if we plan to visit the Colosseum one day and the Vatican a different day, and it rains on the day we go to the Colosseum, that’s not great. By keeping it open, we can watch the weather forecast and visit the Vatican on the day it rains and the Colosseum on the day it doesn’t. Unfortunately, by not buying skip-the-line tickets ahead of time, it might mean that we’re waiting in line. With it being off-peak, however, I don’t think it will be too bad. That being said, I’m not certain what off-peak season is like so I’ll just cross my fingers that we’re not making a horrible mistake.

Instead of tediously planning out a bunch of activities, I’m just keeping a list of things we can do, with the thought that we can make those decisions on a day to day basis. Hopefully that will turn out to be the best approach.

What’s The Value of a Hotel Certificate?

Jenn earned her bonus for her IHG Premier card this month which was 5 free night certificates worth up to 60,000 IHG points each. What does that really mean?

Free night certificates are hard to value. As noted earlier in this post, they’re usually only good for one year and they expire. They also have a maximum value that cannot be exceeded. One thing is almost assured, and that is that we will never redeem any of those certificates for a stay at an IHG property that is charging exactly 60,000 points for a stay. Finding that one hotel room that you need at maximum value is very close to impossible.

So what is the actual value for those certificates? For some people, they would try to maximize the value of those certificates by searching for the best hotel and if they have to go out of their way to maximize the value of that certificate, they will. We really use certificates because we need to stay somewhere, often for just one night, and that might mean on a stopover on a long flight. The most important thing to me is location and Jenn likes a free breakfast. Considering how we use certificates, the chances of us getting full value out of our certificates is basically zero.

That being said, we already used one of these certificates to book the Kimpton De Witt in Amsterdam. We have a 25 hour stopover in Amsterdam on our way to Rome and this checked a lot of boxes for us. It was a short train ride from the airport, right by the train station and downtown by the canals. We were going to have to leave for the airport too early for breakfast, so the fact that they didn’t have free breakfast is irrelevant. This hotel is going for 47,000 points per night, so we used almost 80% of the full value of the certificate. Honestly, that is about as good as you can reasonably expect. The cash value of the hotel room was $302, so I’m not mad about the free night.

For the sake of simplicity, I just value certificates at half of their maximum value. So if I can get a hotel room worth more than 30,000 IHG points with one of these certificates, I’ll be happy. With IHG points being worth around half a cent each, I would say the sign up bonus that Jenn earned was 150,000 points at .5 cents or $750. Considering the first certificate we used saved us $300, I think we’re already ahead.

US Bank Triple Cash

I signed up for the US Bank Triple Cash Rewards Business Card. This is a card with no annual fee. It earns 3% cash back on gas, EV charging stations, office supply stores, cell phone providers and restaurants. It earns 1% cash back on everything else. There is also a $100 per year credit for recurring software purchases, like Quickbooks.

The signup bonus is $750 after spending $6,000 in 6 months. I’m always a big fan of having some extra time to complete a spending requirement, so 6 months is great. This bonus will give us a little cash back to pay for some of those annoying taxes and surcharges when booking award flights.

American Airlines Aviator Red

I also signed up for the American Airlines Aviator Red card, under the assumption that it was going to disappear and this was my last chance to get the 70,000 American Airlines miles bonus for just one purchase and a paying the $99 annual fee. It’s just too easy to pass up. I already met the requirements now and I’m just waiting for those sweet, sweet AA miles to show up in my account. For more information about that card, read my post.

On To The Point Check

We did a pretty good job this last month continuing to use the bonus categories on some of our existing credit cards which led to a total of 6.3% return on all of our spend not devoted to earning a signup bonus.

Card Used

Spend

Points Earned

Point Value

Points Per $

Return on Spend

Amex Gold

$592

1,862

$37.28

3.1

6.3%

Ink Cash

$558

2,772

$56.83

5.0

10.2%

Venture

$547

1,094

$20.24

2.0

3.7%

Wyndham Business

$352

1,955

$21.51

5.6

6.1%

Citi

$297

667

$12.01

2.2

4.0%

Amex Business Gold

$190

546

$10.92

2.9

5.8%

Total

$2,536

8,898

$158.78

3.5

6.3%

This month’s spending not devoted to earning a signup bonus

Aside from the spending in the above chart, Jenn spent around $4,300 on her IHG Premier card earning her 19,000 IHG points and the signup bonus of 5 free night certificates worth up to 60,000 points per night. I spent a little over $500 on my US Bank Triple Cash card earning around $13 in cash back. At the end of the month, we were left with:

293,000 Amex Membership Rewards Points

214,000 Chase Ultimate Reward Points

139,000 IHG Points (includes 4 free night certificates)

104,800 American Airlines Miles

84,700 Capital One Venture Miles

71,900 Marriott Bonvoy Points (Includes 2 free night certificates)

43,000 Wyndham Points

30,400 Citi Thank You Points

11,300 Hyatt Points (includes a free night certificate)

The ability to transfer American Express Membership Rewards Points to Hawaiian Airlines is no longer available. However, this article is an example of what is possible if you are creative with your points and miles.

Recently, I transferred 18,000 American Express Membership Rewards points to Hawaiian Airlines, then transferred them from Hawaiian Airlines to Alaska Airlines to book a round trip positioning flight on American Airlines for my wife Jenn and I. To anyone other than a hardcore travel hacker that seems insane. Yet, to hackers, that sounds like a normal rational decision.

This process was actually rather easy, but there is a lot to unpack in that sentence. Doing this has only really been possible for a few days, and for me it is the result of learning a lot about travel hacking over the course of the last few years. A recent merger between Alaska Airlines and Hawaiian Airlines is the reason why this is suddenly possible.

What is a Positioning Flight?

A few months ago, we booked a trip to Italy using Flying Blue miles to fly KLM to Rome from Chicago and we booked United Airlines to fly back to Chicago from Rome. The problem is that we live 3 hours away from Chicago O’Hare Airport. The reason why we booked it out of Chicago is that the flights were much cheaper than out of our home airport, Quad Cities International.

A one-way ticket from Chicago to Rome was 20,000 Flying Blue miles and $122, but if you tack on the Quad Cities to Chicago leg, it becomes 53,000 Flying Blue miles and $127. It seems insane that from Chicago to Rome was 20,000 Flying Blue miles but adding the leg from Moline to Chicago was 33,000 miles. I’m not doing that.

We were okay with driving to O’Hare, but we didn’t want to. Instead we (originally) used American Airlines miles to book a separate flight from the Quad Cities to Chicago that would save us the drive. Those flights were 7,500 American Airlines miles per passenger each way, or a total of 30,000 American Airlines miles. This is called a positioning flight because we had a separate booking to position us to the airport we wanted to fly out of.

What is a Transfer Partner?

Transfer partners are basically what makes the points in banks’ reward programs so powerful. The reason why people covet Amex Membership Reward points or Chase Ultimate Reward points is that they can be transferred to various airline and hotel programs. Having transferable points lets you keep your points flexible while you’re earning them and then choose the best way to use them when you are redeeming those points.

American Express Membership Rewards have a number of transfer partners. One of those transfer partners is Hawaiian Airlines. You can transfer your Membership Rewards points to Hawaiian Airlines at a rate of 1:1 with a minimum of 1000 points transferred. American Express does charge an excise tax of 60 cents per 1000 points transferred.

OK, But you Booked with Alaska Airlines Not Hawaiian Airlines

Alaska Airlines has been an amazing program for a long time. According to their website, they partner with 31 different airlines. You can redeem Alaska miles for flights on many of them, when they are available. There have been several times that I’ve used Pointsyeah.com to find the best award flight, and Alaska has had the best price.

The problem with Alaska Airlines was that it was hard to amass a lot of miles in their program. There are only a couple of credit cards issued by Alaska, and the signup bonuses are lackluster. They also, until recently, haven’t had any transfer partners. They did, recently, sign a deal with Bilt Rewards to be a transfer partner, but Bilt doesn’t have signup bonuses so amassing a stash of Bilt Rewards points can be difficult.

Nevertheless, when Alaska Airlines and Hawaiian Airlines agreed to a merger, they made an agreement to allow transfers between the two programs. This opened up a back door to move points from American Express Membership Rewards to Alaska miles through Hawaiian. This is fantastic, because amassing a large number of American Express Membership Rewards points is not difficult.

Exact Flights, Different Prices

One of the most consistently baffling things to me about points and miles is the fact that sometimes the same flight is being offered by different programs at different prices. In this case, we had an American Airlines flight booked with American Airlines miles leaving on a Sunday night and returning on a Sunday night. Using American Airlines miles it was 30,000 AA miles and around $22 in taxes for the two of us.

When we originally booked with American Airlines, I saw that Alaska had the same flights for 4,500 points and around $18 per person per flight, so in other words, 18,000 Alaska miles and around $72 in taxes and fees. At the time, I didn’t have access to Alaska miles.

When the backdoor transfer option from American Express to Alaska Airlines materialized, I checked to see if that was still available and it was so I jumped on it. American Airlines has free cancellations, so it wasn’t a difficult to have my points and fees returned.

Saving American Airlines Miles

One big reason that we changed how we booked this flight was being able to use something other than American Airlines miles. American Airlines doesn’t have any transfer partners and lately it seems like whenever I’m comparing prices on award flights American Airlines always has competitive pricing. I didn’t want to use AA miles that I find so valuable if I don’t need to.

Also, earning 30,000 AA miles using just credit card spend requires a lot of spending. If we did it using the Barclays Aviator Red card, all purchases except American Airlines purchases earn 1 point per dollar spent. That means I would have to spend $30,000 on that credit card to earn 30,000 points.

On the other hand, I transferred 18,000 American Express Membership rewards points to Alaska and those are much easier to earn. When I buy groceries or dine out using my American Express Gold Card, I earn 4 Membership Rewards points per dollar spent on that card. That means I would only need to spend $4,500 on that Amex Gold Card, assuming I only use it for groceries and dining out, to earn the 18,000 miles necessary to book the flight. That’s a huge difference! Yes, the Alaska flights cost an extra $50 in fees but I was happy to spend that to keep those 30,000 AA miles.

Will This Back Door Transfer Option Remain?

It is unclear at this point whether transferring American Express Membership Rewards points through Hawaiian to Alaskan Airlines will remain an option. We know that transferring points between Hawaiian Airlines and Alaskan Airlines will be around for the foreseeable future. This has created a lot of interest in the travel hacking community for Hawaiian Airlines credit cards.

In the past, most travel hackers weren’t very interested in Hawaiian Airlines credit cards. Hawaiian miles weren’t worth a whole lot and because of that, the credit cards weren’t interesting. In fact, the Points Guy used to value Hawaiian miles at .9 cents per point and Alaskan miles at 1.5 cents per point. Moving 100,000 Hawaiian miles to Alaska Airlines increases their value, according to these valuations, by $600. That’s a big deal.

The problem for American Express is that now this throws their agreement with Hawaiian out of balance. If Hawaiian miles are suddenly worth more, will Hawaiian Airlines/Alaska Airlines demand more money to sell those miles to American Express? I don’t know, and there has been a lot of speculation in the travel hacking community that this transfer agreement could end.

The potential end of this agreement has me tempted to move some Membership Rewards to Alaska, but I don’t really have enough to just move them without a flight in mind. Instead, I think I’ll just wait and hope that Membership Rewards continues to allow transfers to Hawaiian Airlines. That being said, I might just be looking at a Hawaiian Airlines credit card soon. It’s never a bad idea to take advantage of a great deal when it pops up.

Last week an article by CNBC indicated that Citigroup was in heavy negotiations with American Airlines to be the exclusive card issuer for American Airlines credit cards. These negotiations are immensely important for American Airlines because the revenue that comes from airline loyalty programs are now a huge portion of their income. It’s become so important, in fact, that it’s sometimes joked that airlines are credit card companies that fly planes. According to Delta CEO Ed Bastian, nearly 1% of the entire US economy is charged to Delta credit cards. The revenue from selling loyalty points to banks is a multi-billion dollar industry for airlines, and its a revenue stream they take very seriously.

American Airlines is in a strange situation because they have cobranded credit cards issued by two different banks. There are four credit cards issued by Citigroup which include three personal credit cards and one business card. Barclays technically has two personal American Airlines cards, but one is only available through upgrade, the AAdvantage Aviator Silver. The only Barclays American Airlines card with a current sign up bonus is the AAdvantage Aviator Red.

The fact that American Airlines has two banks issuing their credit cards is because of an American Airlines merger with US Airways over a decade ago. US Airways had a relationship with Barclays and after the merger US Airways credit cards issued by Barclays became American Airlines cards. American Airlines kept that relationship going, even as people began to forget about US Airways.

It makes sense for American Airlines and Citigroup to form an exclusive relationship. It would make the AAdvantage program more straightforward by reducing the complexity of having multiple card issuers. In the end, I think it’s highly likely that American Airlines will end their relationship with Barclays and form an exclusive relationship with Citigroup.

AAdvantage Aviator Red Card

If Barclays is going to get dropped from the AAdvantage program, it’s safe to say the Barclays AAdvantage Aviator Red card is going to go away. In some respects, good riddance, it’s not a very interesting card. It earns 2 miles per dollar spent on American Airlines purchases and 1 mile on everything else. You do get a free checked bag and preferred boarding but the annual fee is $99.

The thing that does make it interesting is that the signup bonus is incredibly easy to earn. Right now, there is a 70,000 mile signup bonus available through Frequent Miler’s website. What is the spending requirement? Signup and use it once. Literally, pay the $99 annual fee, activate the card and buy a pack of gum using the credit card and 70,000 AAdvantage miles are yours for the taking.

In addition, I’ve been eyeballing some deals to Portugal for spring break that are running around 22,500 AAdvantage miles one way per person. Having an extra 70,000 miles would top off our accounts enough to book the flights there, even though it wouldn’t be enough to get home.

Fear of Missing Out

I think that this is the last chance I have of taking advantage of one of the biggest no-brainers in points and miles. It’s legitimately buying 70,000 miles for $99. It’s not the best signup bonus the card has offered. Jenn got this card about a year ago when it offered 60,000 points for one charge and 15,000 for an authorized user and an additional charge to the authorized user card. However, it is definitely a solid deal, and waiting for a better deal at this point could mean that I miss out completely.

In the middle of writing this post, I actually did apply for this card and was approved. That’s fantastic and I will happily take my shiny new 70,000 miles from American Airlines. As a matter of fact, after I was approved, my daughter walked downstairs and I convinced her to apply for it as well and she was approved.

In all fairness, when I told her there was an annual fee she balked, but I told her if she would use her miles to pay for her ticket to Portugal, I would pay for her annual fee and she jumped on it.

Potentially Good News From the Exclusive Deal with Citigroup

Knowing that Barclays will likely be cut out of the American Airlines credit card business, it means that there will be less choices, and less available signup bonuses in the future. Still, it does raise the possibility of American Airlines becoming a transfer partner for Citi Thank You points.

American Airlines currently doesn’t have a transfer partner. Most major airlines have transfer partners, with Delta Airlines being a partner from American Express Membership Rewards points and United Airlines and Southwest Airlines being partners from Chase Ultimate Reward points. American Airlines was briefly a transfer partner of Citi Thank You points a few years ago, and was a transfer partner of Bilt Rewards very recently. A few months ago Bilt Rewards and American Airlines ended that partnership, and maybe that has to do with their negotiations with Citigroup.

With no current transfer partner, and with American Airlines negotiating a deal with Citigroup, there is a fairly good possibility that Citi Thank You points will become transferable to American Airlines. If that becomes a reality, I will definitely be attempting to earn more Citi Thank You points, because I find a lot of value in American Airlines miles.

In the end, I hope the changes that American Airlines makes to their credit card business with Citigroup works out to be beneficial to both them and their cardholders. Knowing how important that loyalty points are to the business of airlines puts a lot of pressure on them to have a good and profitable loyalty program. In the meantime, I need to figure out how I’m going to use these shiny new American Airlines miles.