In what is becoming a new family tradition, to celebrate our niece, Zoey graduating from high school, we are going to Europe to celebrate. Well, not really we, since I’m not going, but Jenn and her sister Misty are taking Zoey and our daughter Emma to Europe this summer.

It is, however, my responsibility to do a lot of the trip planning. The parameters were fairly loose. It needed to be in mid-July. Jenn wanted to take Misty to Munich because she will absolutely love Munich, and maybe a day trip to Neuschwanstein Castle. Zoey wanted to travel to Dublin or Italy.

So, I got on my laptop and started to search on PointsYeah.com, thinking that this wouldn’t be that hard since they were pretty flexible. To my horror, there wasn’t anything that was very good. Almost everything was over 40,000 points one-way per person in economy for flights that were less than desirable. A lot of them had taxes and surcharges of well over $200 per ticket – for economy flights out of the US!

What surprised me the most was that typically you can count on Flying Blue to have flights available from Chicago throughout Europe on KLM or Air France for 25,000 points and a little over $100 each. Those deals were no where to be seen.

Flying United Airlines with Partner Miles

I was beginning to notice that United had a number of flights available for 40,000 points. I wasn’t interested at 40,000 points, but I also know that is the saver fare price for a flight to Europe and sometimes those saver fares end up on partner websites. Maybe I should check those partner sites?

Turkish Airlines

I’ve used Turkish Miles and Smiles to book United flights before. In our case, I used it to book flights to San Jose del Cabo Airport for 10,000 miles from Chicago. That is no longer a thing, because the new price after devaluation is 30,000 points. I wasn’t expecting this to be very good because the devaluation has made most of their partner awards more expensive, but I thought I should look. Sure enough, it was 55,000 miles instead of 40,000. Not worth it.

Air Canada Aeroplan

Next I checked out Air Canada Aeroplan and found the same flight for 40K points and $80 CA ($56 USD). This is the same number of points but about $50 more expensive for taxes and fuel surcharges. This might actually make sense to do, because Aeroplan transfers from Amex, Capital One, Chase and Bilt whereas United miles only transfer from Chase. So if you can’t come up with United miles, this might make some sense. 40,000 points still seemed to steep for me, though.

Avianca Lifemiles

Avianca Lifemiles does have quite a few partner redemption options and that is why it’s good to check them as well. They had the flight listed at 40,000 miles and $28.50, which is still a little more than United at 40,000 miles and $5.60. However, like Air Canada, you can transfer to Avianca Lifemiles from more programs than United does. Avianca transfers from basically everyone including Amex, Capital One, Chase, Citibank and Wells Fargo. If you’re too short on Chase points or United miles, Avianca Lifemiles might make sense.

Singapore Airlines

I had basically forgotten about Singapore Airlines. I always found it difficult to find any availability on their website when I was looking. I decided to try them anyway and yes, that flight was available. They had four tickets available at 30,500 Krisflyer miles each and $5.60 for taxes. That’s great! Singapore Airlines also transfers from Amex, Chase, Citibank and Capital One, making it easy to get enough points.

What I Ended up Booking

So obviously on the way there I booked the United flight direct from Chicago to Munich for 30,500 points transferred from Citibank and $5.60. I will be booking a connecting flight from Munich to Dublin on Aer Lingus for 7,500 Avios transferred from American Express and $53. The return flight from Dublin to Chicago was also booked on Aer Lingus with American Express Membership Rewards transferred to Avios for 20,000 points and $155. So each complete itinerary was a total of 58,000 points and $204.

When I priced out the entire itinerary as a multi-city cash flight with United Airlines it was $1,550 per ticket. That means that the 58,000 points saved around $1,350 or about 2.3 cents per point. I’m always happy to get over 2 cents per point, so I’m happy with this redemption and that wouldn’t have been possible without remembering that I could redeem Singapore Airlines Krisflyer miles for United saver award flights. In the end it saved us a total of 38,000 transferable points.

Finding United Flights on Singapore Airlines website

The only flights that will normally be available on partner sites like Singapore Airlines will be saver awards. It is also important to note that not all saver awards will be available to partner websites. If you are looking to book one of these saver awards on a partner airline, you need to find when one should be available.

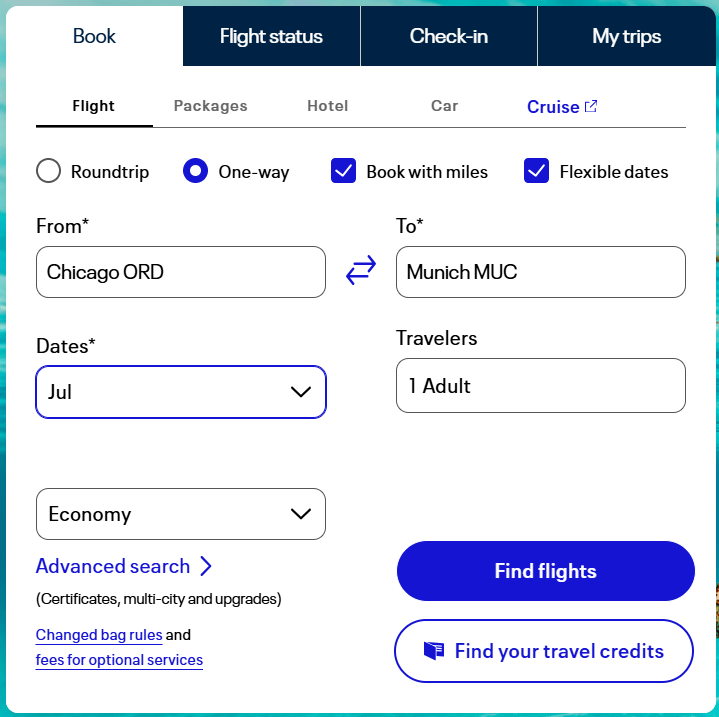

The best way is to go United.com and DON’T SIGN IN. The reason that you shouldn’t sign in is that if you have a United credit card, you have access to additional award inventory. This will not be available to partner websites. You’re looking for basic saver awards.

What you want to do is search for flights, but make sure you check the checkboxes for one-way, book with miles, and flexible dates. As soon as you hit search it will prompt you again to sign in – DO NOT DO IT, just click on the ‘x’ in the corner.

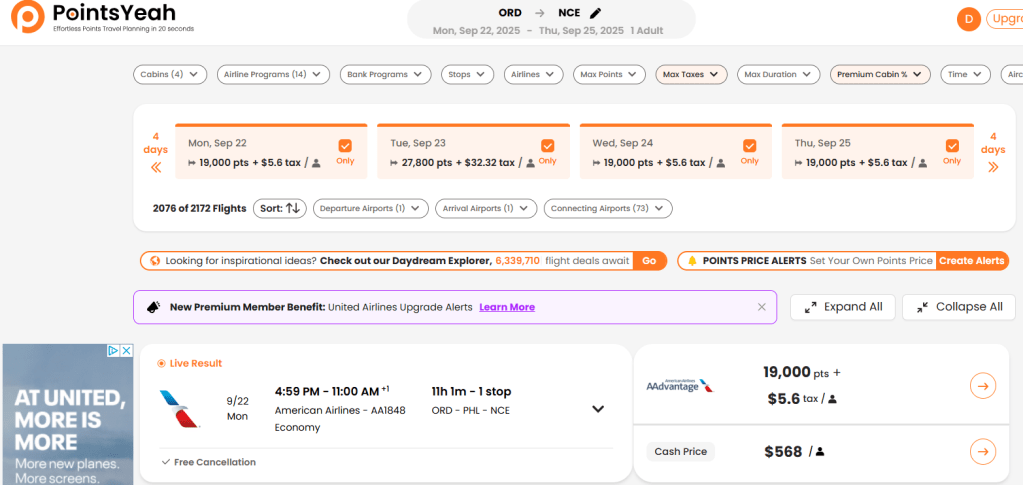

In this case, I see a ton of available flights for 40k + $5.60. When you look below on one specific flight, you see “Saver Award” listed for this day. Looking at this, I would assume that it’s likely that there are a ton of available flights in July from Chicago to Munich on United that I should be able to find on Singapore Airlines Krisflyer.

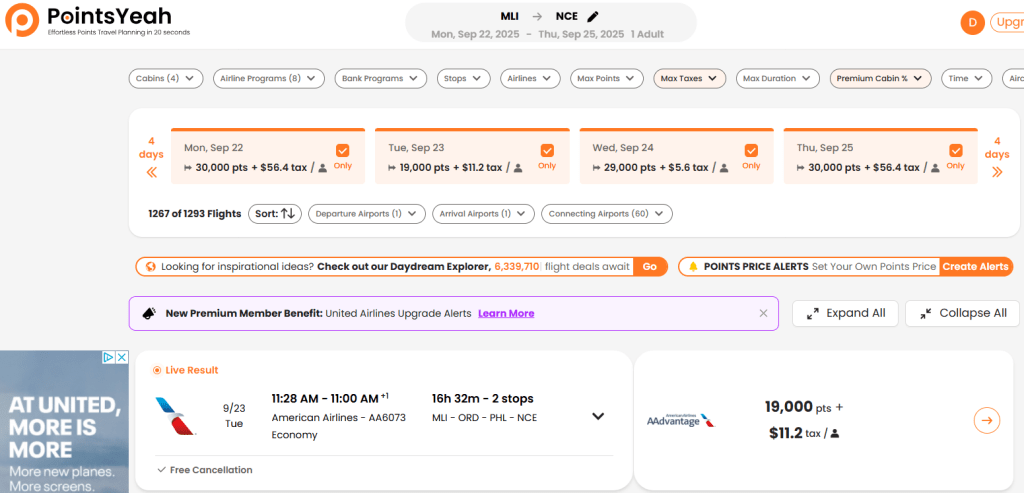

If you then go to the Singapore Airlines website and search for award flights from Chicago to Munich for that date, at first you won’t find anything. That’s because the default is to search Singapore Airlines flights. You need to click on the Star Alliance tab in order to find anything from United Airlines.

Not only will you find wide open availability on United for July, as was indicated by saver awards on the United website, but you also see flights for Lufthansa as well. That is because Lufthansa is also a Star Alliance member. The number of points is the same as the United flights because Singapore Airlines has a standard award chart that has North America to Europe as that number of points. The difference, however, is the amount of taxes and fees that are required to book that flight. On United, it’s $5.60 and with Lufthansa it’s $316.50 and has a stop in Frankfort. Yeah, I think I’ll take the United flight.

When To Book United on Partner Sites

So this is when things can get complicated. Earlier in this post, I mentioned four different ways to book the same United Airlines flight from Chicago to Munich. In my analysis, Singapore Airlines was the cheapest and so I booked with them. The problem is that Singapore Airlines will not be the cheapest all of the time. Each of these programs have different award charts that mean that depending on where you are flying, different programs might be the ideal for that particular flight.

Some of these award charts are regional, and some are distance based. For each of these charts, they define regions differently or they are using different cut-offs for distance. I’m not going to go into the different award charts here, but I want to show what it’s like for those of us who routinely use Chicago Ohare airport to demonstrate just how different it can be.

| Chicago to: | United Airlines | Singapore Airlines | Air Canada Aeroplan | Avianca Lifemiles | Turkish Airlines |

| Munich | 40,000 miles and $5.60 | 30,500 miles and $5.60 | 40,000 miles and $56 | 40,000 miles and $28.50 | 55,000 miles and $5.60 |

| Tokyo | 60,000 miles and $5.60 | 59,500 miles and $164.50 | 50,000 miles and $56 | 55,000 miles and $28.50 | 75,000 miles and $5.60 |

| Cancun | 20,000 miles and $47.47 | 19,500 miles and $47.47 | 12,500 miles and $98 | 15,000 miles and $58 | 30,000 miles and $47.47 |

| Honolulu | 25,000 miles and $5.60 | 19,500 miles and $5.60 | 22,500 miles and $44 | 25,000 miles and $15.20 | 10,000 miles and $5.60 |

| Auckland | 55,000 miles and $40.90 | 66,000 miles and $40.90 | 60,000 miles and $92 | 60,000 miles and $36.93 | 100,000 miles and $40.90 |

| Denver | 8,800 miles and $5.60 | 14,000 miles and $5.60 | 10,000 miles and $33 | 15,000 miles and $5.60 | 10,000 miles and $5.60 |

In the above chart, you will notice that even though these are identical United Airlines flights, they have wildly different prices. That is because of the award charts that each of these programs use. If you are aware of these price differences and check on multiple websites, you can save a lot of points as well as money on taxes and fuel surcharges.

In addition, these programs have different transfer partners, which might affect your decision as well. In the case of the Denver flight, the lowest price is 8,800 miles and $5.60 but the miles are United miles which only transfer from Chase. If you don’t have any United miles or Chase Ultimate Reward points, you might decide that 10,000 Turkish Miles and Smiles is better for you because you can transfer those points from Citi Thank You points or Capital One Venture miles. If all you have is American Express Membership Reward points, you might want to use Air Canada Aeroplan, even though the taxes are higher, because you can transfer to Air Canada from Amex.

Think Before You Book a United Flight

I enjoy flying United. I haven’t yet had a bad United flight. Generally the seats have been comfortable and the planes have been in good shape. I know that’s not the case for everyone, but I’ve had pretty good luck on United. That being said, I find that booking award flights with United to be generally overpriced, although I love that they don’t tack on huge fuel surcharges on their award flights.

In addition to the fact that their award prices can be elevated, the fact that their only transfer partner is from Chase makes it sometimes difficult to amass the amount of points necessary for those flights.

Understanding how and when to use partner awards for those flights can save you a ton of points and might mean the difference between being able to make the trip at all. Keep in mind, you don’t need to memorize the award charts to make this work. All you need to do is when you identify a saver award flight on United, remember that you might be able to book that flight on partners like Turkish Airlines, Singapore Airlines, etc. Then start looking for that flight on other sites and see if you can find a better deal for you. This one little trick can make a huge difference in the price of identical flights.